BROCK MID-SESSION COMMENTS

NO NEW RECOMMENDATIONS

Grain and oilseed futures remain higher at mid-day as the markets regain a little of the ground lost in the wake of Monday’s bearish USDA reports. Fresh export demand and strong weekly ethanol output are supportive factors. Corn is up 2 to 3 cents, and soybeans are up 4 to 8 with nearby months leading the way. Wheat is up 1 to 4 cents. Cotton, which had risen the past couple of days, is down slightly. Rice futures are unchanged in most-active March.

In outside markets, the Dow is down about 250 points, and the dollar index is down 0.2%. Crude oil is up 70 cents despite a surprising build in U.S. stocks, with support coming from ongoing concern about a U.S. attack on Iran. For the second time in four business days, investors this morning looking for a ruling by the U.S. Supreme Court on President Trump’s tariffs were disappointed, as the court issued two rulings on other cases.

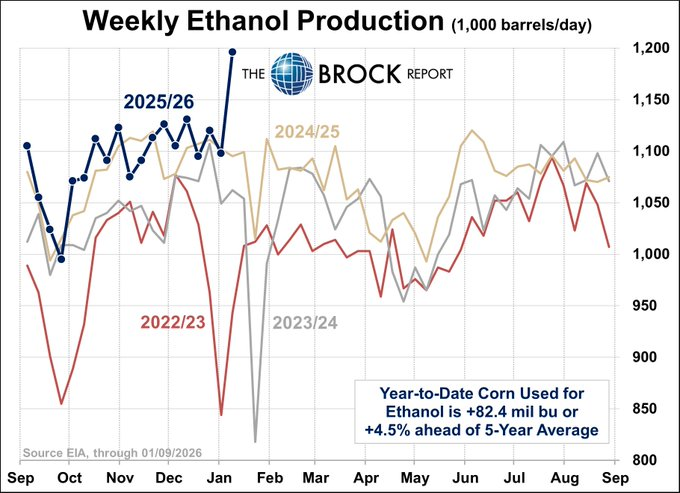

Despite the bearish news from USDA this week, demand has been a bright spot for corn, and that story continued this morning as EIA reported weekly ethanol production shooting to a record high. Ethanol output in the week ended Friday was 1.196 million barrels per day, up from 1.098 million the prior week. The four-week average is up 2.1% from a year ago. The total easily beat the prior weekly record high, set in mid-December, at 1.131 million barrels per day. Strong exports have been a driver for the industry, and EIA reported exports averaging 119,000 barrels per day in the week ended Friday, up from 113,000 the prior week. The four-week average of 150,000 is up from 136,000 a year ago. Ethanol stocks expanded to 24.5 million barrels as of Friday, up from 23.7 million the prior week, but still down 2.1% from a year ago.

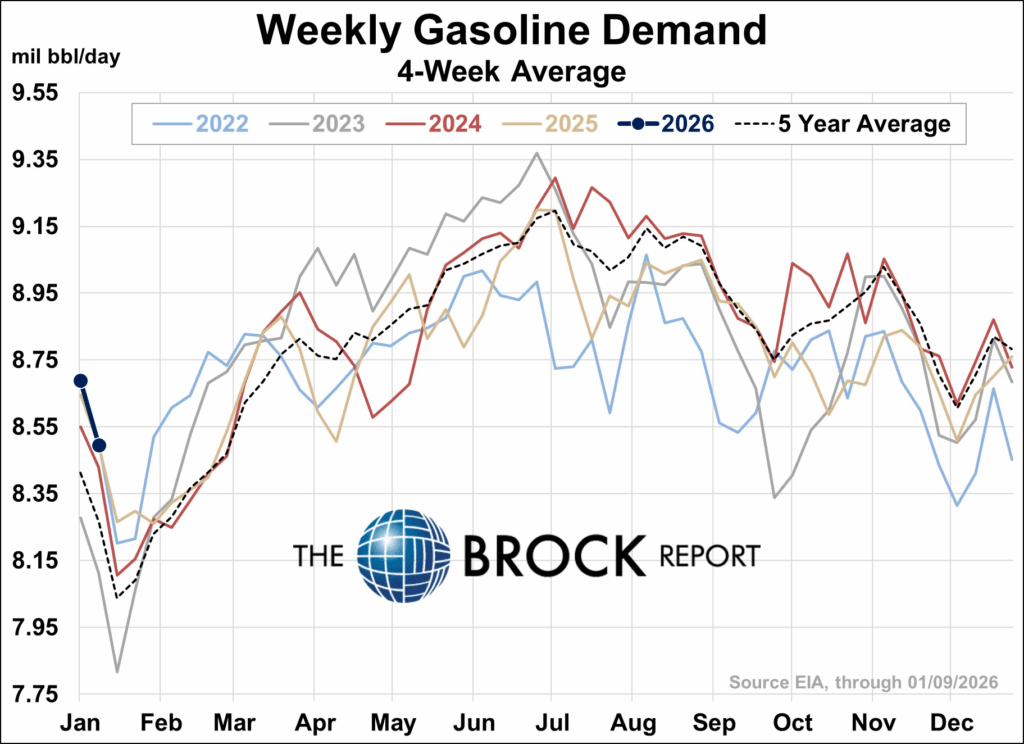

Gasoline demand averaged 8.304 million barrels per day in the week ended Friday, up from 8.170 million the prior week. The four-week average is flat versus a year ago. Crude oil stocks expanded to 422.4 million barrels, up from 419.1 million the prior week and up 2.4% from a year ago. Analysts were on average expecting a drawdown of 1.7 million barrels.

Not much new happening with South American weather, which is not good news for corn and soybean prices. In Argentina, recent light rainfall provided only temporary relief in drier western and southern areas, but additional rounds of showers over the next two weeks should prevent sharp deterioration according to World Weather Inc. Central and northern Argentina remain mostly well supplied with moisture. In Brazil the favorable pattern continues, with regular rainfall expected across most key growing areas over the next two weeks, helping maintain favorable soil moisture, though slowing fieldwork at times. Southern Brazil should see the least rain overall but has enough moisture in place to support crop development, World Weather says.

As noted this morning, USDA reported two flash export sales: 334,000 metric tons of soybeans to China, and 136,000 metric tons of corn to South Korea. This follows two flash sales of soybeans reported yesterday. There had also been two flash sales of corn reported on Monday.

Wheat futures reached their session highs shortly after reopening this morning on support from speculative short covering, but have since faded under renewed pressure from ample U.S. and world supplies and are near their lows for the day at midsession. Monday’s USDA data may already have been largely factored into the futures market, but the near-term upside for prices looks very limited given the current fundamentals.

Relatively active Russian exports are a negative market factor. Moscow-based analyst SovEcon estimates Russia will export 3.0-3.5 MMT of wheat during January, up from just 2.3 MMT in January 2025.

Dry conditions in the U.S. HRW wheat belt remain a potential bullish market factor. A dry-biased weather pattern will continue through the next eight days in the region, according to World Weather Inc. Temperatures will trend colder this weekend, but no significant cold is expected yet. Some warming will occur again next week ahead of what will likely be a more-aggressive cold air mass that could arrive around Jan. 22 or Jan. 23. There is some uncertainty as to how cold the region will become later this month, but there may be a need for protective snow cover in some areas.

LIVESTOCK COMMENTS

NO NEW RECOMMENDATIONS

Livestock futures are mixed at 11:10 a.m. CT, with lean hog futures ranging from 5 cents lower to $1.43 higher, while live cattle futures are $1.15 to $2.05 lower and feeder cattle futures are $1.65 to $2.55 lower. Front-end lean hog futures are finding further support from demand optimism and technically-driven speculative buying. Live cattle and feeder cattle futures are feeling some pressure from speculative profit taking in the wake of Tuesday’s strong gains.

Nearby Feb. lean hog futures have traded to a 4-session high of $86.10 and are near their session high. Nearby resistance for Feb. hogs is at $86.35-$86.50, with support at $83.78-$84.30. April lean hogs have broken out to a 3-month-plus high of $92.70, while June lean hogs have broken out to a new contract high of $105.25 after establishing nearby chart support at $103.93. We are sticking with our hedge positions in April, June and Aug. futures for now, but will probably look to exit those positions if today’s strength holds.

The composite pork cutout value was 12 cents lower at midmorning at $91.68. USDA again did not report midmorning negotiated cash carcass values due to packer confidentiality reasons. The weighted avg. price of hogs sold under swine/pork market formula agreements at midmorning was $80.26, up 43 cents vs. Tuesday morning. The lagging CME cash lean hog index is 10 cents lower at $80.50, and is expected to fall another 11 cents on Thursday. Today’s hog slaughter is expected to run 493,000 head, up 5,000 from last week, and 9,000 vs. last year. The avg. pork packer operating margin is estimated by HedgersEdge at $16.90 per head, down from $18.85 on Tuesday.

Feb. live cattle futures have dipped through nearby chart support at $235.15-$235.19, trading as low as $235.05, with next support at $233.95, while last week’s low is key support down at $231.13. April futures are trading inside of their Tuesday range, but are near their session low of $236.96 with nearby resistance at $239.05 and nearby support at $236.23 and $236.05. Most-active Mar. feeder cattle futures earlier hit a 12-week high of $362.90, but are now near their session low of $358.80, with nearby chart support at $356.18.

Plains direct cash cattle markets remain quiet this morning with no packer bids or feedlot asking prices reported. We expect significant trade will not develop until Thursday or Friday. Steady to higher trade is still favored as most showlists appear to be smaller and wholesale beef prices have been strengthening, although packer margins remain very poor, which will limit demand. Beef cutout values were 33 cents to $1.34 higher at midmorning, with the choice cutout value at $359.33. The avg. beef packer operating margin is estimated by HedgersEdge at minus $202.75, up from minus $207.00 on Tuesday.

BROCK MARKET POSITIONS

CORN: Cash-only Marketers: 2024 CROP:100% sold on hedge-to-arrive contracts and regular forward contracts (7-19-23, 8-15-23, 1-2-24, 5-8-24, 5-15-24, 5-16-24, 5-30-24, 11-12-24, 12-12-24, 2-5-25, 2-21-25, 6-5-25, 6-20-25).

2025 CROP: 40% sold on hedge-to-arrive contracts (2-5-25, 2-24-25, 6-9-25, 7-9-25, 1-9-26).

Hedgers: 2024 CROP: 100% sold on hedge-to-arrive and regular forward contracts (7-19-23, 8-15-23, 5-8-24, 5-16-24, 11-12-24, 12-12-24, 2-5-25, 2-21-25, 4-15-2025, 6-5-25, 6-20-25).

2025 CROP: 40% sold on hedge-to-arrive contracts and regular forward contracts (2-5-25, 2-24-25, 6-9-25, 7-9-25, 1-9-26); aside futures; short July 2026 $5.40 call options against 10% (6-6-25).

SOYBEANS: Cash-only marketers: 2024 CROP: 100% sold (7-19-23, 8-22-23, 11-16-23, 5-16-24, 10-8-24, 12-18-24, 2-5-25, 2-12-25, 2-26-25, 6-2-25, 6-23-25).

2025 CROP: 50% sold on hedge-to-arrive contracts or regular forward contracts (2-12-25, 6-23-25, 7-9-25, 9-2-25, 11-4-25, 12-1-25).

Hedgers: 2024 CROP: 100% cash sold (7-19-23, 8-22-23, 11-16-23, 5-9-24, 12-18-24, 2-5-25, 2-26-25, 4-15-25, 4-29-25, 6-2-25, 6-23-25).

2025 CROP: 50% sold on hedge-to-arrive contracts or regular forward contracts (2-12-25, 6-23-25, 7-9-25, 9-2-2025, 11-4-25, 12-1-25), aside futures, long $10.50 February put options on Mar. 2026 futures against 20% (1-9-26).

SRW WHEAT: Cash-only Marketers: 2025 CROP: 80% sold on hedge-to-arrive and regular forward contracts (5-30-24, 6-4-24, 10-15-24, 2-24-25, 6-9-25, 6-10-25, 6-24-25, 11-6-25), aside futures. 2026 CROP: No sales advised.

Hedgers: 2025 CROP: 70% sold on hedge-to-arrive and regular forward contracts (5-30-24, 10-15-24, 2-24-25, 6-9-25, 6-10-25, 6-24-25, 11-6-25);. 2026 CROP: No sales advised.

HRW WHEAT: Cash-only Marketers: 2025 CROP: 80% sold on hedge-to-arrive and regular forward contracts (5-30-24, 6-4-24, 10-15-24, 2-24-25, 6-9-25, 6-10-25, 6-24-25, 11-6-25).

Hedgers: 2025 CROP: 70% sold on hedge-to-arrive and regular forward contracts (5-30-24, 10-15-24, 2-24-25, 6-9-25, 6-10-25, 6-24-25, 11-6-25); aside futures. 2026 CROP: No sales advised.

LEAN HOGS: Short April 2026 lean hog futures against 25% of 1st qtr. marketings (1-12-26), June 2026 lean hog futures against 25% of 2nd qtr. marketings (1-12-26) and Aug. 2026 lean hog futures against 25% of 3rd and 4th qtr. marketings (1-12-26). Long January $81 put options on Feb. 2026 lean hog futures (12-17-25), short $108 call options against June 2026 lean hog futures (1-2-26). Aside futures.

LIVE CATTLE: Aside futures and options.

FEEDER CATTLE: Feeder sellers are aside futures. Feeder buyers remain aside futures.

MILK: No forward cash sales advised; aside futures.

FEED BUYERS: CORN: No forward cash purchases advised. SOYMEAL: 100% of 1st qtr. needs bought in the cash market; 50% of 2nd qtr. needs bought in the cash market (1-7-26).

COTTON: Cash-only Marketers: 2024 CROP: 100% sold (2-12-24, 2-27-24, 4-3-24, 6-27-24, 6-28-24, 3-13-25, 3-18-2025, 4-28-25, 6-24-25, 7-16-25). 2025 CROP: 10% sold in the cash market (9-17-25).

Hedgers: 2024 CROP: 100% cash sold (2-12-24, 2-27-24, 4-3-24, 6-27-24, 3-13-25, 3-18-25, 4-28-25, 6-24-25, -16-25), aside futures: 2025 CROP: 10% sold in the cash market (9-17-25). Aside futures.

RICE: 2024 CROP: 100% sold (5-3-24, 5-8-24, 5-28-24, 5-29-24, 7-15-2024, 7-30-24, 9-24-24, 2-21-25. 4-29-25, 7-18-25). 2025 CROP: 10% forward contracted (6-9-25).

NOTE: Along with the potential for profit, there is always a risk of losing money when trading futures and options contracts.

Copyright 2026 by Richard A. Brock & Associates, Inc.

Any unauthorized redistribution or reproduction of this commentary is strictly forbidden.