Maybe. This is not the headline anyone wants to read, and not one that we want to write either. We are far from saying definitively that this is the absolute top of the year but there are enough flashing lights going on this week that we all should give this additional thought.

More on that below, but first I want to cover what has been an interesting week to say the least. For me, this was a week that I transitioned from our Destin, Florida office to our Milwaukee office. I decided to make a long (1,400 miles) road trip out of it. Left Sunday morning and drove to Cleveland, Mississippi. Spent two nights there visiting with clients and looking at crops during the day. Great experience and adds a new perspective to my thought process. From central Mississippi on Tuesday I transitioned to Saint Louis, Missouri spending a night there and then on Wednesday afternoon, drove from there on up to Milwaukee, Wisconsin.

Along the way I was able to see a considerable amount of planting going on. We’re in the heart of planting cotton in the Mississippi Delta and planters were running everywhere, as well as crop dusters flying to drop granular fertilizer. From Saint Louis to Milwaukee, driving up through the eastern half of Illinois, planters were also busy planting corn and soybeans. Planting is off to a fast start for corn, and particularly soybeans and rice. Cotton is right on its usual pace, but there are no significant issues in the U.S. anywhere, yet.

Also spent time speaking with the manager at one of the largest grain terminals in Mississippi, where a considerable number of Mississippi Delta and Louisiana farms deliver corn and soybeans. One comment he made was somewhat alarming. While this individual had managed this terminal for several years, he stated that he had the least amount of corn and soybeans booked for new-crop delivery that he can ever remember. Farmers have not been selling corn or soybeans in that area. Concerning. We’ve heard the opposite in other parts of the country, where it seems farmers are aggressively selling into these higher prices. Perhaps this is anecdotal, perhaps it’s representative of the broader trends.

To give a little more substance to the discussion of price outlook and why it’s concerning that producers have not been making sales, let’s take a quick look at where prices have been. Since January 1, here are some facts:

1. July soybeans have rallied from $10.65 to $12.20, a 14% increase.

2. July corn futures have rallied from $4.60 to $5.10, an 11% increase.

3. July wheat rallied from $5.30 to $6.60, a 25% increase.

4. July cotton has rallied from $0.66 to $0.84, a 27% increase.

My guess is very few of us thought we would see prices this spring where they are. One rule of thumb that old-time grain traders have always told us that we should keep in mind: spring rallies in corn and soybeans should be sold. Look back in history. The market usually gives us some opportunity, but most of us come up with reasons for not making the sales.

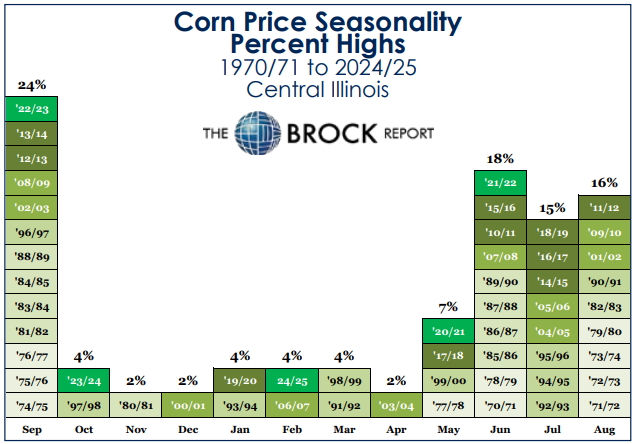

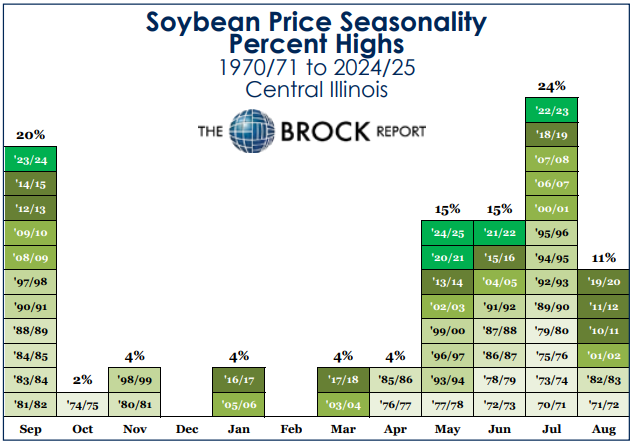

One of those reasons is the seasonal charts (listed below) that we so often share, which show increased odds of the marketing year high happening in June and July. Those highs are typically caused by planting problems or early growing season weather concerns. Whether those concerns actually cause yield issues is beside the point, premium gets built into the market. Bottom line, marketing year highs in May have happened in the past, and considering how this rally has been largely fueled by Iran and the energy market, it’s not unreasonable to think a resolution to the conflict could cause the highs to occur in May this year.

Some Facts to Keep in Mind

What we want in life and what we get in life are sometimes not the same thing. What we want in grain prices and what we get in grain prices are also often different. We need to be careful not to set our targets too high but make our decisions relative to the expected fundamental average expected price, and to the technical action taking place. With that said, consider the following:

1. A driver in the bull market for grains in the last two months primarily has been crude oil because of the war in Iran. No one knows exactly how or when this is going to end. But it will at some point. Crude oil established a technical sell signal this week. That has been a driver behind soybean oil which has provided the support for soybeans. This whole relationship is starting to unravel.

2. The crops are getting planted quickly. As pointed out below, progress is on par or well ahead of normal in every crop, particularly for soybeans, particularly in the south (see page 8).

3. Corn futures established an outside week down this week in most active July and in December. While they closed well off the week’s lows, July failed at the March highs and Dec. failed at $5.00. That’s a strong signal that the corn market is making a top.

The rally has pushed prices to a level where many producers are at break-even or above in corn, soybeans, wheat and cotton. No one is going to get rich at these levels, but the losses will be minimal. The only sure loser at this price level is Mississippi Delta corn farmers.

Break-even in the Delta is over $6.00 per bushel on corn because of higher fertilizer application prices as well as insecticides and herbicides in that area of the country. Very expensive to raise corn there. And unlike the Corn Belt, many producers there had not covered their fertilizer needs prior to the outbreak of war in the Middle East.

For specific strategies, read the advice on the following pages. But across all of these markets, the old rules of thumb will apply. When in doubt, sell something and hope you’re wrong. Prices are much better than many were expecting in corn, soybeans, cotton and wheat. If you advance sales here and the market continues higher, that’s fine. If you don’t and the market turns lower, that’s not.

Another advantage these markets have this year is that corn prices are running at near 70% of carry. Hedge in March futures and storage will pay. Soybeans are still an inverted market. The market wants soybeans, but those spreads are starting to change. That is a strong indicator that we should not be hanging on to old-crop soybeans. Volatile markets are also emotional markets. But volatility creates profit opportunities. It’s an interesting time.

Sidebar: Something New

While it hasn’t been a perfect correlation, quite often recently the answer to, “why are grain prices doing what they are doing?” has been “headlines out of the Middle East.” That remains a major wildcard, posing a risk for traders in either direction. But we will get some fresh news in the coming week.

First, on Tuesday, USDA releases its first balance sheets for 2026-27 in its monthly Supply and Demand report.

The other news will be out of China, where President Trump is set to meet Xi Jinping Thursday. Right now, there are hopes for some new China soybean purchase commitments but, overall, expectations for the meeting are low. While many people are assuming China is being hurt the most since over 90% of their fuel comes through the Strait of Hormuz, the reality is that China has large supplies of oil on hand as with corn and soybeans. They hoard commodities to protect themselves in risky markets such as is occurring in Iran now. A deal with the U.S. may rely more on goodwill than desperation.