LEADING OFF: Grain and oilseed futures are mostly firm this morning: Corn is up 2 to 3 cents, and wheat is up a penny. Soybeans are up 3 to 4 cents, after initially seeing follow-through overnight to Monday’s bearish outside day lower. Soybean oil also posted a bearish outside day down on Monday, and is down 20 points this morning. Cotton futures are mixed, but rose to fresh highs for the move overnight, including the highest price for front-month cotton in nearly two years.

In outside markets, crude oil is down $3 in the May and $1 to $2 in other contracts, with pressure from news that Iran was considering pausing shipping through the Strait of Hormuz to avoid derailing peace talks with the U.S. The U.S. blockade of the strait continues, but a Chinese ship reportedly passed through the blockade, and Saudi Arabia is pressing the U.S. to end the blockade. While the situation remains very far from settled, the bottom line right now is still that both the U.S. and Iran are looking at ways to de-escalate. The dollar index is down 0.4% this morning, which could be a supportive factor for the grains, and gold is up about $30. Major equity index futures are pointed slightly higher.

Corn could get a boost on the re-opening on fresh export sales. USDA this morning reported a sale of 120,000 metric tons to unknown destinations for the current marketing year. It also reported a sale of 316,000 metric tons to Mexico, with 65,000 of that for the current year, 139,000 for next year, and 112,000 for 2027-28.

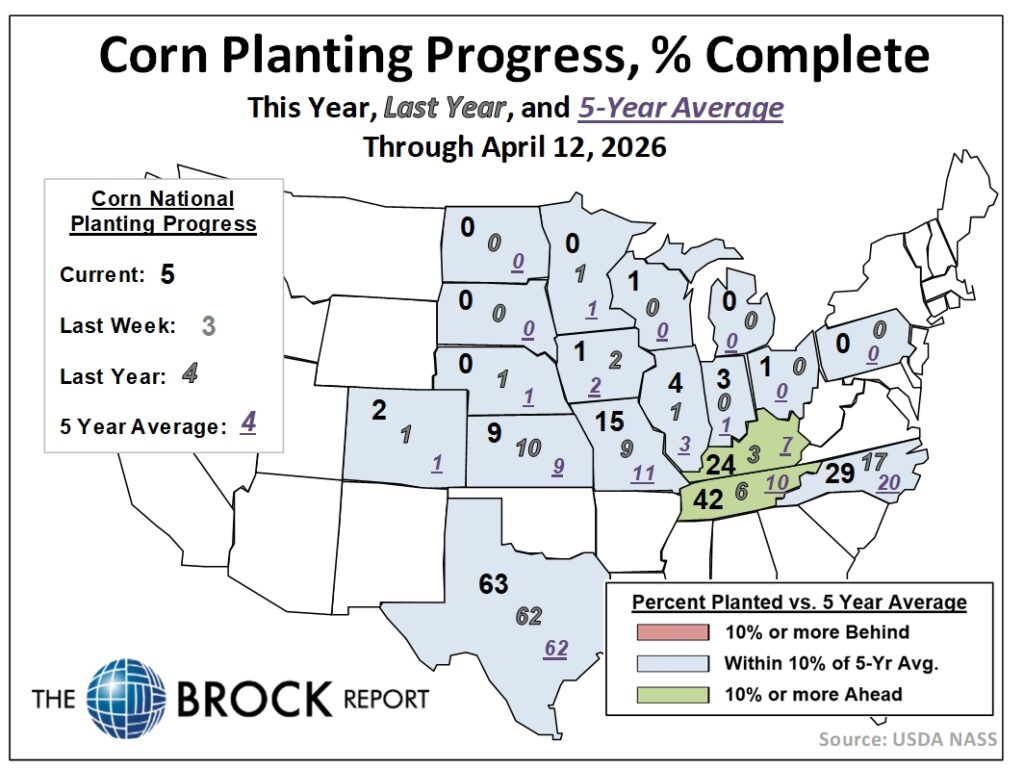

CORN: Rain and storms blew across the Upper Midwest overnight, and much of Illinois is seeing rain this morning, with more of that to come over the next five days and beyond from central Texas through eastern Kansas, into Iowa and the Great Lakes region. This will keep any early corn planting progress slow, although if the rains give way to a calmer pattern by the end of the month, it will work in most producers’ favor. The region can use the rain.

USDA yesterday afternoon pegged U.S. corn planting progress at 5%, up from 3% last week and above the 5-year average of 4% but behind the avg. trade estimate of 6%. Planting continued to move swiftly in the Mid-South. Tennessee planting progress was at 42% vs. a 5-year average of 10% and Kentucky progress was at 24% vs. an average of 7%. Illinois was 4% planted vs. an average of 3%, while Indiana was 3% planted vs. an average of 1% and Iowa was 1% planted vs. an average pace of 2%.

South American weather is mixed, with some ongoing concern about excessive rains in much of Argentina. Some areas of southern Brazil are also wet, although that is generally welcome given dryness there this season. Central and northern areas of Brazil are entering a drier pattern as the monsoon season fades.

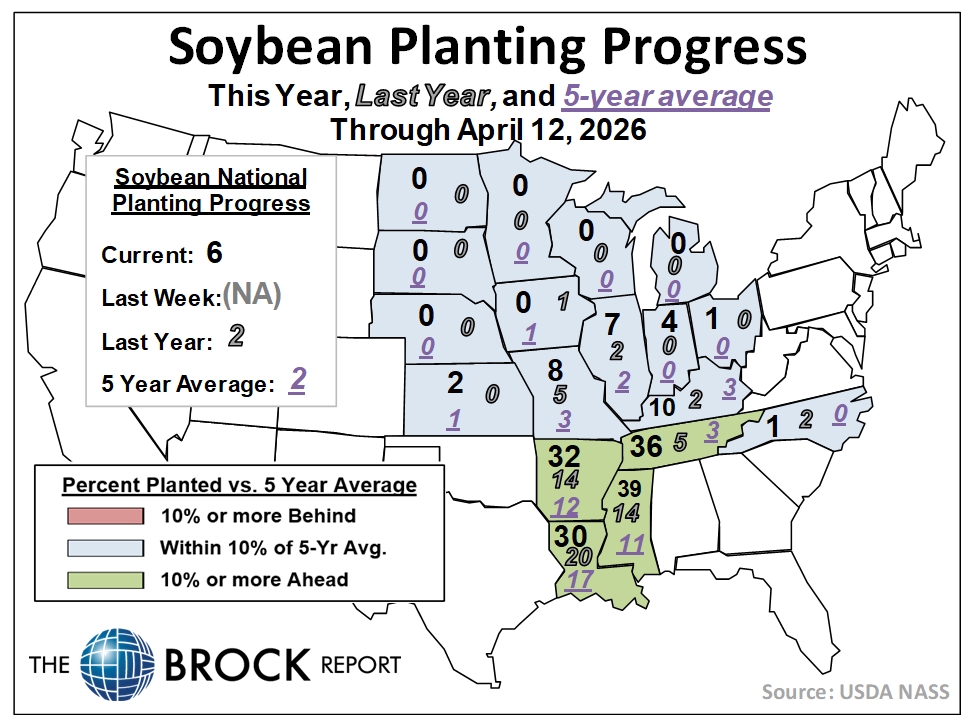

SOYBEANS: USDA yesterday afternoon reported U.S. soybean planting progress of 6%, versus the five-year average of 2%. The fast early progress may add to speculation about larger soybean plantings. Most of activity was in the Delta and Midsouth, with Louisiana 30% planted vs. a 5-year average of 17%, Mississippi 39% planted vs. an average of 11%, Arkansas 32% planted vs. an average of 12% and Tennessee 36% planted vs. an average of 3%. Dry conditions are expected to persist across the South through at least the next week, exacerbating what is already a severe drought. So while the planting pace should remain good, concerns about the crop’s potential will grow until the weather pattern shifts.

China’s soybean imports in March were up 14.9% year-over-year, but well below analyst expectations due to delayed shipments from Brazil tied to tougher quality inspections. Imports of 4.02 MMT were up from 3.5 MMT a year earlier, data from the General Administration of Customs showed. Reuters quotes one Chinese analyst saying that it was expecting 6.4 MMT. Last year’s volumes were lower because of a delayed Brazil harvest and because buyers were shying away from U.S. beans.

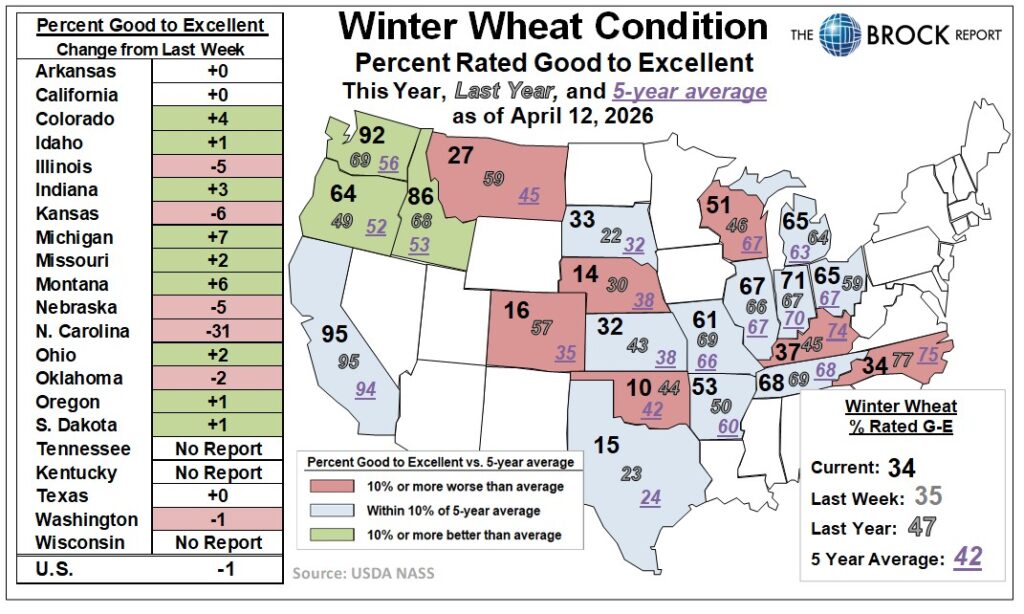

WHEAT: Monday’s Crop Progress report showed the winter wheat condition following nationally to 34% good/excellent, down a point from last week. The trade was on average expecting it to hold steady. While there was improvement in several soft red winter wheat states, key hard red winter states saw a further decline: Nebraska was down 5 points to 14% good/excellent, Oklahoma was down 2 points to 10%, and Kansas was down 6 points to 32% good/excellent. There also was a 31-point drop in North Carolina, to 34% good/excellent. Colorado did see a four-point gain to 16%, and among soft red winter states, Indiana, Illinois, Ohio and Michigan all reported improvement, and are near their five-year averages.

LIVESTOCK: Lean hog futures were mixed in a choppy trading session yesterday, but the chart picture remains poor given last week’s bearish outside week down. Our sell-stop in July futures was not hit Monday, but we may maintain a similar stop today. Hedgers should keep alert for possible fresh advice. June futures posted their lowest close since Jan. 2 on Monday. The market’s 200-day moving avg. is potential support at $102.05-$102.10, with the next level of support below that at $100.00.

June live cattle futures traded inside of their Friday range to start the week but finished near their session low after failing to take out Friday’s high at $249.95 in early trading. There is no indication the market has topped out again, but June futures may be vulnerable to pressure from speculative profit taking ahead of Friday’s USDA report as they remain technically overbought. Slow movement of cattle to slaughter also remains a negative market factor. May feeder cattle futures may be poised to test their contract high at $376.63.