GRAIN COMMENTS

NO NEW RECOMMENDATIONS

Grain and oilseed futures are mostly higher at mid-day on technical buying and strength in crude oil. Corn is up 8 to 9 cents, and wheat is up 5 to 7. Soybeans are up 22 to 24 cents and are approaching Monday’s highs, led by the soybean oil, which has soared by 4%, or around 275 points. Cotton is down slightly, and rice is slightly higher.

In outside markets crude is surging anew today, up by about $4.50, despite an IEA plan for its largest release of strategic reserves in its 50-year history. Gold is down $60 to $70, and the dollar index is up 0.45%. The Dow is down about 500 points.

The monthly CPI report for February was up 2.4% from a year ago, in line with expectations and in line with a month earlier. The “core” CPI, which excludes food and energy, was up 2.5%, also in line with expectations. Food prices were up 3.1%, the biggest year-over-year increase since August. But this report seems trivial in light of the war between the U.S. and Iran that has since broken out, and there is widespread agreement that the Fed will now take a wait-and-see approach to see how the war affects prices and inflation, without considering this February report.

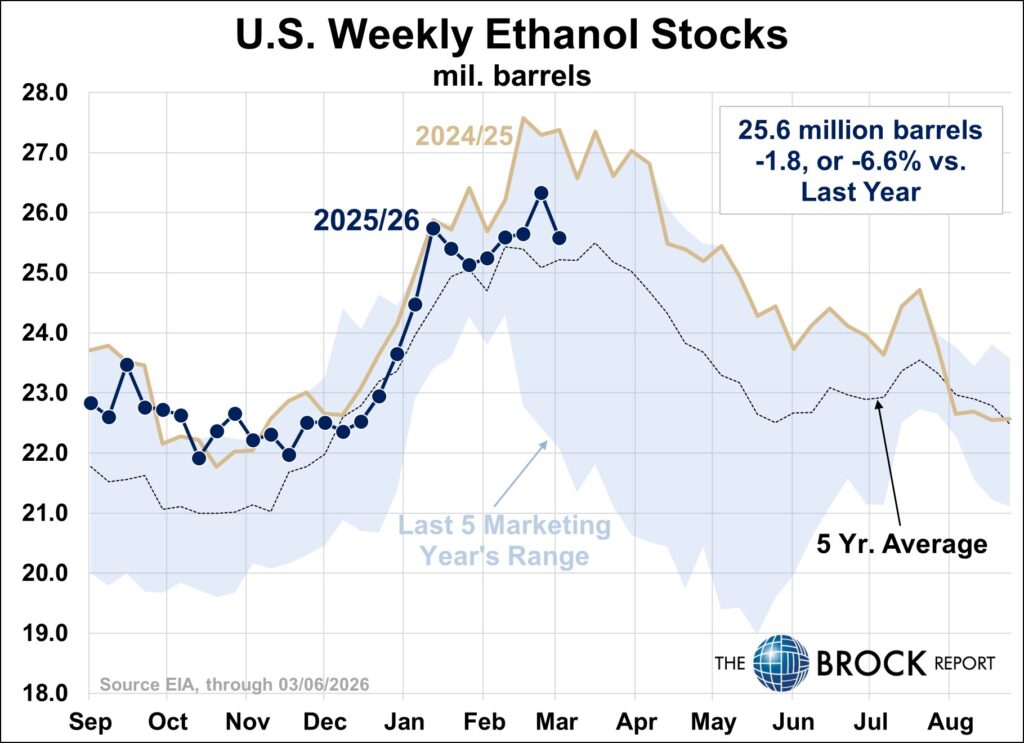

Weekly ethanol output of 1.126 million barrels per day was down from 1.095 million the prior week. The four-week average is up 3.6% from a year ago. Ethanol stockpiles of 25.6 million were down from 26.3 million the prior week, and down 6.6% from a year ago. Ethanol exports of 188,000 barrels per day were down from 217,000 the prior week, but the pace remains well ahead of a year ago: the four-week average of 181,000 is up from 135,000 a year ago.

Gasoline demand of 9.241 million barrels per day was down from 8.292 million the prior week, and the four-week average is up 0.8% from a year ago. Crude oil stocks of 443.1 million barrels were up from 439.3 million the prior week, and up 1.8% from a year ago.

South American weather looks mostly favorable, with southern Brazil being a notable exception. World Weather Inc. notes that the Safrinha crop is getting planted outside the ideal window, and also into dry conditions that are expected to intensify in the coming weeks. It says that “conditions for the crop will often be poor” and that some growers will pick other crops. However, central and northern Brazil will continue to see good conditions with plenty of rain. In Argentina, rains Friday and Saturday in southeastern Brazil will be much-welcome and proceed broader rains across the country from Sunday through Wednesday. The rains could reverse some recent declines in yield potential in dry southeast areas, World Weather says. Yesterday USDA lowered its Argentina corn crop estimate by 1 MMT to 52 MMT, while raising its Brazil estimate by 1 MMT to 132 MMT.

Wheat futures have been boosted by strength in corn and soybean futures amid renewed concerns about the U.S.-Iran war and strength in crude oil futures following Iranian drone attacks on ships in an around the Strait of Hormuz. Concerns about export demand are likely a negative market factor, with the war boosting ocean freight and insurance rates.

May SRW wheat futures have traded inside of their Tuesday range and now have nearby chart support at $5.89 1/4 and $5.83 3/4, with nearby resistance at $6.04 1/4-$6.04 1/2. May HRW wheat futures now have nearby resistance at $6.23 1/2, with nearby support at $6.07 1/4 and $5.98 1/4.

In export news Algeria’s state grains agency OAIC is believed to have bought 150,000-200,000 MT of optional-origin milling wheat in a tender for restricted shipment to two ports only that closed on Tuesday.

Precipitation in the U.S. southern Plains over next two weeks will still be quite limited, which will maintain concern over dryland crop development potentials. A big, but brief surge of unusually cold air Sunday into Monday may burn back some recent wheat development in the south, but no permanent damage is expected. Frost and freezes at this time of year are helpful in keeping wheat development in check until significant rain evolves. A high pressure ridge in the second week of the outlook will be responsible for more unusual warmth and dryness.

LIVESTOCK COMMENTS

NO NEW RECOMMENDATIONS

Livestock futures are lower across the board at 11:35 a.m. CT amid renewed concerns about the U.S.-Iran war and higher crude oil prices. Live cattle and feeder cattle futures are also under pressure from weaker cash markets. Lean hog futures are 45 cents to $1.68 lower, while live cattle futures are $2.48 to $2.58 lower and feeder cattle futures are $5.78 to $7.60 lower. Trading is likely to remain highly volatile, with the latest developments in the war continuing to influence prices.

April lean hog futures are near their session low of $95.25, with further support down at $94.10 and nearby resistance at $96.33-$96.63. July lean hogs gapped lower on this morning’s open and now have nearby chart resistance at $112.40-$112.43, with major resistance remaining at $113.33-$113.38. July hogs have traded as low as $111.15 and have nearby support at $110.65.

The midmorning composite pork cutout value was 72 cents lower at $98.38. The weighted avg. price for hogs sold under swine/pork market formula agreements was 23 cents lower at $91.18. The lagging CME cash lean hog index is 10 cents higher at $90.97 and is expected to rise another 23 cents on Thursday. Today’s hog slaughter is expected to run 492,000 head, up 4,000 vs. last year.

Live cattle futures opened lower this morning and have extended losses since. Most contracts are near their session lows. Nearby resistance for April live cattle have traded as low as $229.63 with nearby chart support at $227.33, while nearby resistance is at $231.80 and $233.05. Most-active April live cattle futures have fallen to a 2-month-plus low of $342.03 and have nearby chart support at $341.00 and nearby resistance at $347.80.

There is light trade reported in Plains direct cash cattle markets this morning, with DTN reporting sales of 900 head in Nebraska at $235 on a live basis and $372 on a dressed carcass basis, along with sales of 200 head in Kansas at $235 live, $5 lower than last week’s market. USDA reported Tuesday negotiated sales of 7,274 head in Nebraska on Tuesday at mostly $372 dressed, down $8 from last week’s market. Minimal Tuesday negotiated sales of 257 head were reported in Kansas at $235 live.

The avg. beef packer operating margin is estimated by HedgersEdge at minus $10.45 per head, up from minus $45.50 on Tuesday. Beef cutout values ranged from $1.27 to $1.85 higher at midmorning, with the choice cutout value at $395.94.

BROCK MARKET POSITIONS

CORN: Cash-only Marketers: 2025 CROP: 60% sold (2-5-25, 2-24-25, 6-9-25, 7-9-25, 1-9-26, 3-6-26).

2026 CROP: 10% forward contracted (3-6-26).

Hedgers: 2025 CROP: 60% sold (2-5-25, 2-24-25, 6-9-25, 7-9-25, 1-9-26, 3-6-26); aside futures; short July 2026 $5.40 call options against 10% (6-6-25).

2026 CROP: 10% cash forward contracted (3-6-26). Long April $4.80 short-dated new-crop put options against 10% (3-6-26); long May $4.80 short-dated new-crop options on 10% (3-9-26).

SOYBEANS: Cash-only marketers: 2025 CROP: 80% sold on hedge-to-arrive contracts or regular forward contracts (2-12-25, 6-23-25, 7-9-25, 9-2-25, 11-4-25, 12-1-25, 2-13-26, 2-20-26, 3-6-26).

2026 CROP: 20% sold on forward contracts (2-20-26, 3-6-26).

Hedgers: 2025 CROP: 80% sold on hedge-to-arrive contracts or regular forward contracts (2-12-25, 6-23-25, 7-9-25, 9-2-2025, 11-4-25, 12-1-25, 2-13-26, 2-20-26, 3-6-26); aside futures.

2026 CROP: 20% sold in the cash market on forward contracts (2-20-26, 3-6-26); long April $11.30 short-dated new-crop put options against 10% (3-6-26).

SRW WHEAT: Cash-only Marketers: 2025 CROP: 100% sold on hedge-to-arrive and regular forward contracts (5-30-24, 6-4-24, 10-15-24, 2-24-25, 6-9-25, 6-10-25, 6-24-25, 11-6-25, 1-28-26, 2-1-26, 2-25-26), aside futures. 2026 CROP: 20% sold on forward contracts (3-6-26)

Hedgers: 2025 CROP: 100% sold on hedge-to-arrive and regular forward contracts (5-30-24, 10-15-24, 2-24-25, 6-9-25, 6-10-25, 6-24-25, 11-6-25, 1-28-26, 2-1-26, 2-25-26); 2026 CROP: 20% cash forward contracted (3-6-26). Aside futures.

HRW WHEAT: Cash-only Marketers: 2025 CROP: 100% sold on hedge-to-arrive and regular forward contracts (5-30-24, 6-4-24, 10-15-24, 2-24-25, 6-9-25, 6-10-25, 6-24-25, 11-6-25, 10-28-26, 1-28-26, 2-1-26, 2-25-26). 2026 CROP: 20% sold on forward contracts (3-6-26).

Hedgers: 2025 CROP: 100% sold on hedge-to-arrive and regular forward contracts (5-30-24, 10-15-24, 2-24-25, 6-9-25, 6-10-25, 6-24-25, 11-6-25, 1-28-26, 2-1-26, 2-25-26); aside futures. 2026 CROP: 20% cash forward contracted (3-6-26). Aside futures.

LEAN HOGS: Short April 2026 lean hog futures on 25% of 1st qtr. marketings and 50% of 2nd qtr. marketings (2-9-26, 2-12-26), short July 2026 lean hog futures on 50% of 3rd qtr. marketings (2-12-26); short Oct. 2026 lean hog futures on 50% of 4th qtr. marketings (2-12-26).

LIVE CATTLE: Aside futures.

FEEDER CATTLE: Feeder sellers are short Aug. feeder cattle futures against 25% of 2nd qtr. and 25% of 3rd qtr. marketings (3-3-26). Feeder buyers remain aside futures.

MILK: No forward cash sales advised; aside futures.

FEED BUYERS: CORN: 100% of first qtr. needs covered in cash market. SOYMEAL: 100% of 1st qtr. needs bought in the cash market; 100% of 2nd qtr. needs bought in the cash market (1-7-26); 25% of 3rd qtr. needs covered in cash market (2-12-26).

COTTON: Cash-only Marketers: 2024 CROP: 100% sold (2-12-24, 2-27-24, 4-3-24, 6-27-24, 6-28-24, 3-13-25, 3-18-2025, 4-28-25, 6-24-25, 7-16-25). 2025 CROP: 20% sold in the cash market (9-17-25, 2-26-26).

Hedgers: 2024 CROP: 100% cash sold (2-12-24, 2-27-24, 4-3-24, 6-27-24, 3-13-25, 3-18-25, 4-28-25, 6-24-25, -16-25), aside futures: 2025 CROP: 30% sold in the cash market (9-17-25, 2-26-26). Aside futures.

RICE: 2024 CROP: 100% sold (5-3-24, 5-8-24, 5-28-24, 5-29-24, 7-15-2024, 7-30-24, 9-24-24, 2-21-25. 4-29-25, 7-18-25). 2025 CROP: 30% sold (6-9-25, 1-28-26, 2-10-26).