CORN COMMENTS

NO NEW RECOMMENDATIONS

Corn futures edged 1/4 cent to 1 cent lower under pressure from further weakness in soybean futures and somewhat disappointing export data. Crude oil futures weakness and a firm dollar were also negative market factors, while slow cash corn movement helped limit futures weakness. Mar. futures fell 1 cent to $4.43 3/4, while May futures fell 1 cent to $4.51 1/4 and July fell 3/4 of a cent to $4.57.

Corn futures started out the week where they left off last year, chopping around in narrow ranges with traders awaiting tomorrow’s monthly USDA Supply/Demand report. Mar. futures have held in a range of 10 1/2 cents over the past 7 sessions. Futures remain in short-term uptrends, but for Mar. corn, a close below $4.39 3/4 would now break the uptrend. Mar. corn has nearby resistance at $4.41 3/4-$4.42 1/2, with nearby resistance at $4.47 1/4 and at $4.52 1/4 and key resistance at $4.55-$4.57.

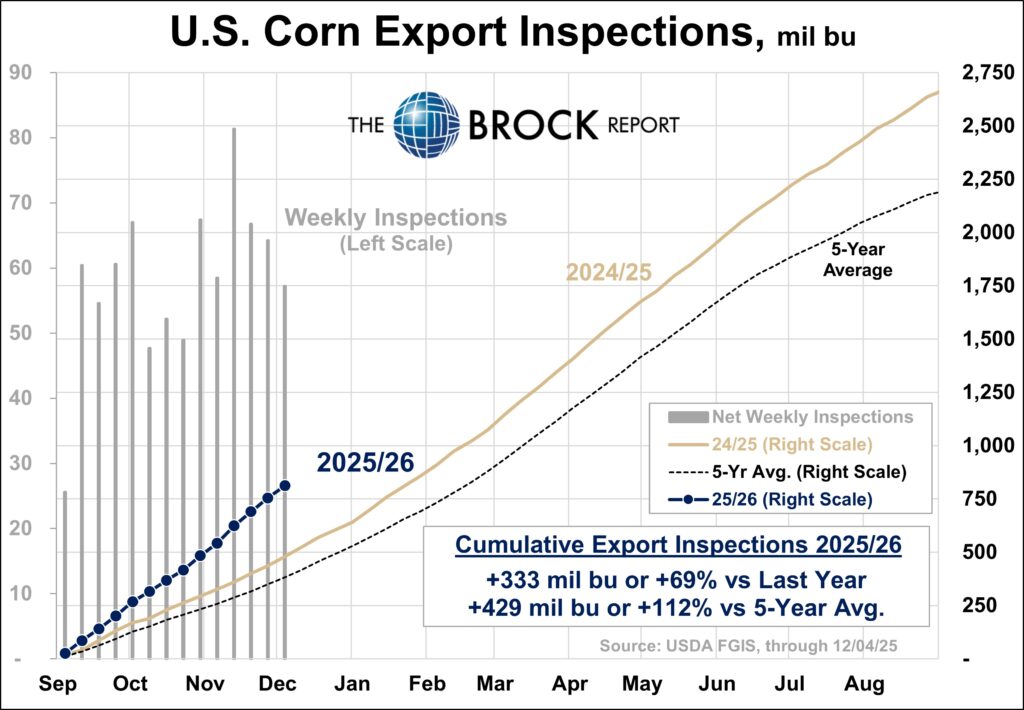

Export demand for U.S. corn remains strong, but today’s export data did not provide any fresh fodder for demand bulls. U.S. corn export sales for the week ended Dec. 4 totaled 57.2 mil. bu., down from 64.2 mil. a week earlier and 42.1 mil. a year earlier. Export inspections for the marketing year to date were still tremendously strong at 812.2 mil. bu., 69.4 mil. above a year earlier. Delayed export sales data for the week ended Nov. 6, pegged net U.S. corn export sales for that week at only 38.6 mil. bu., down from the previous week’s 77.6 million. Export sales for the year to date as of Nov. 6 were still 30.7% above a year earlier.

Ahead of tomorrow’s USDA report, trade estimates of the 2025-26 U.S. corn carryout average 2.146 bil. bu., just 8 mil. below USDA’s November estimate in a range from 2.037-2.370 bil. bushels, according to a Bloomberg News survey of 24 analysts. USDA could potentially raise its forecasts for U.S. corn exports further based on the fast pace of sales and shipments. On the negative side, it could potentially lower its forecast for 2025-26 feed/residual use. USDA did not lower that estimate in November, despite lowering old-crop feed/residual use.

USDA today released its baseline supply/demand projections thru 2025, calculated for budget purposes, based on November data. USDA projected 2026 corn plantings of 95 mil. acres, down from 98.7 mil. in 2025, with harvested acreage at 86.9 mil., down from 90.0 mil. this year, with production at 15.815 bil. bu., down from 16.752 bil. this year on a yield of 182 bu., down from 186.0 this year. Total 2026-27 corn use is projected to fall to 15.975 bil. bu., down from 16.155 bil. this marketing year, with exports at 3 bil. bu, down from 3.075 this year. USDA estimated the 2026-27 corn carryout at 2.019 bil. bushels vs. 2.154 bil. this year.

Central Illinois spot processor basis bids range from 16 cents under Mar. futures to par with the board, according to USDA. CIF basis bids for delivery of corn to the U.S. Gulf are steady to stronger vs. Friday afternoon. The CIF bid for December delivery is 11 cents stronger at 90 over Dec. futures, with the bid for January delivery steady at 81 over Mar. futures, while the bid for February delivery is 1 cent stronger at 82 over.

SOYBEAN COMMENTS

NO NEW RECOMMENDATIONS

Soybean futures sold off for the fifth time in 6 sessions, posting losses ranging from 1 3/4 to 11 1/2 with nearby Jan. futures weakest under pressure from declining expectations for Chinese export demand and prospects for large S. American production. Weakness in soyoil and crude oil futures also weighed on futures. Jan. soybeans fell 11 1/2 cents to $10.93 3/4, while Mar. futures fell 10 1/4 cents to $11.05 3/4 and May fell 8 3/4 cents to $11.16 3/4. Most-active Jan. soyoil futures fell 51 points to 51.18 cents, while Jan. soymeal futures fell $1.10 to $306.30.

The soybean futures chart picture has become downright ugly with 2025-crop contracts falling through their 40-day moving avg. for the first time since Oct. 20 and posting their lowest closes since Oct. 30. Futures are now technically oversold heading into tomorrow’s USDA report, but there are no indications they are near a bottom after they closed near their session lows. Jan. soybeans now have no chart support above the upward gap left on their daily chart at $10.63-$10.70 1/4 on Oct. 27. The market continues to have a valid downside objective of $10.60, based on the head-and-shoulders top on its daily chart. There’s also a chart gap on the weekly soybean futures continuation chart at $10.45-$10.52 1/4 that the market may target.

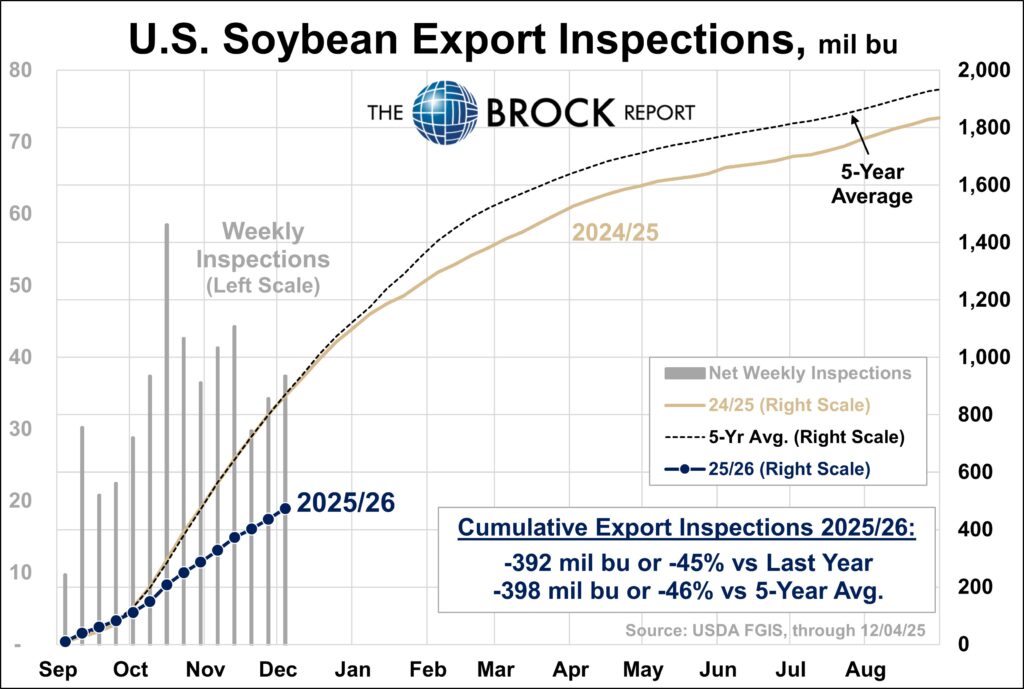

USDA reported U.S. soybean export inspections for the week ended Dec. 4 at 37.4 mil. bu. up from 34.3 mil. a week earlier, but down from 63.9 mil. a year earlier. U.S. soybean export inspections for the marketing year to date totaled 474 mil. bu., down 45.2% vs. a year earlier. The report showed modest inspections of 4.405 mil. bu. for China. Delayed soybean export sales data for the week ended Nov. 6 was disappointing, showing soybean sales of only 18.9 mil. bu., down from 45.9 mil. a week earlier. China was a buyer of 8.25 mil. bu. on the week. U.S. soybean export sales for the marketing year to date totaled 650.6 mil. bu., down 39.7% from a year earlier.

Trade expectations for the 2025-26 U.S. soybean carryout ahead of tomorrow morning’s USDA report avg. 306 mil. bu., 16 mil. bu. above USDA’s November estimate in a range from 250-385 mil. bushels, according to the Bloomberg survey. Estimates of Brazil’s 2025-26 soybean crop avg. 175.4 MMT in a range from 175.0-177.2 MMT vs. USDA’s November estimate of 175.0 MMT. Estimates of Argentina’s crop avg. 48.6 MMT, just 100,000 MT above USDA’s November estimate.

USDA’s baseline projections for budget purposes, based on November data peg 2026-27 U.S. soybean plantings at 85.0 mil. acres, up from 81.1 this year, with harvested acres at 84.2 mil., up from 80.3 million. U.S. soybean production is forecast at 4.465 bil. bu., up from 4.253 bil. bu. this year on a yield f 53.0 bu, steady with this year. Total use is estimated at 4.460 bil. bu., up 160 mil. from this year on increases in both the U.S. crush and exports, with the carryout seen at 314 mil. bu., up from 290 mil. this year. The 2026-27 avg. on-farm price is pegged at $10.30, down from $10.50 this year.

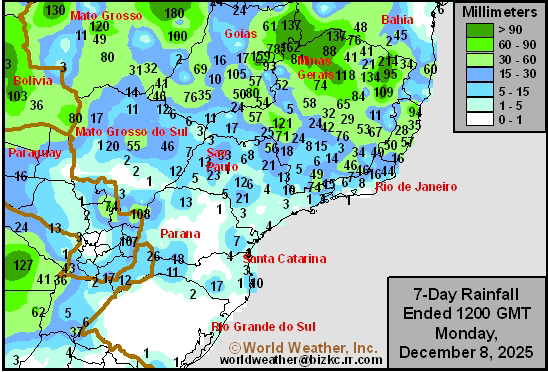

Center-west and northeastern Brazil received significant rain during the past week and the moisture profile improved for Mato Grosso and Goias into Minas Gerais and Bahia, though these areas still need more rain. The biggest change that occurred in the past week was the drying of soil in southern parts of the nation raising the need for widespread rain to restore favorable topsoil moisture there. Wet weather during the next two weeks will gradually bolster soil moisture across much of Brazil. Long-term production potentials will improve for most locations due to the increased rainfall.

Central Illinois processor spot soybean basis bids range from 8 to 5 cents stronger at 10 cents under Jan. futures to 5 cents over, according to USDA. CIF basis bids for delivery of soybeans to the U.S. Gulf weaker compared with Friday afternoon. The CIF basis bid for December delivery is 2 cents weaker at 75 over Jan. futures, while the bid for January delivery is 2 cents weaker at 86 over and the bid for February delivery is 1 cent weaker at 78 cents over Mar. futures.

WHEAT COMMENTS

NO NEW RECOMMENDATIONS

Wheat futures settled lower in listless trade ahead of tomorrow’s USDA report. Chicago wheat settled down ¾ to 1 ½ cents in nearby months, at $5.36 in the December, $5.34 ¾ in the March and $5.42 ¼ in the May. Kansas City wheat settled down 2 ¼ to 4 ¾ cents, at $5.21 in the December, $5.26 ½ in the March and $5.38 in the May. Minneapolis wheat was mostly down 1 to 2 cents, settling at $5.81 ½ in the December, $5.71 ¼ in the March and $5.80 ¾ in the May. Expectations for USDA to raise its estimates of 2025-26 world production and ending stocks were likely a negative market factor today.

Technically, benchmark Chicago March futures are the definition of a sideways market right now. It traded a range of $5.29 ¾ to $5.44 ½ on Dec. 2 and it has stayed within that range since. It traded within that range for several days prior to Dec. 2 as well. If that low doesn’t hold, there’s no clear technical support to prevent a test of the contract low of $5.08 ½, although we do not anticipate that unless tomorrow’s support is surprisingly bearish for wheat or sparks a selloff in corn.

There are few crop problems for wheat right now. Conditions improved over the fall across the U.S., Europe and the former Soviet Union. There are some concerns about excessive moisture in China, but there’s no “crisis” for wheat around the world currently. In the U.S., central and southern Plains will be mostly dry over the next 7 days. Temperatures will be warm through the first half of the week, before a dramatic plunge late this week into the weekend. World Weather says that snow cover should prevent crop damage, but that the situation should be watched closely.

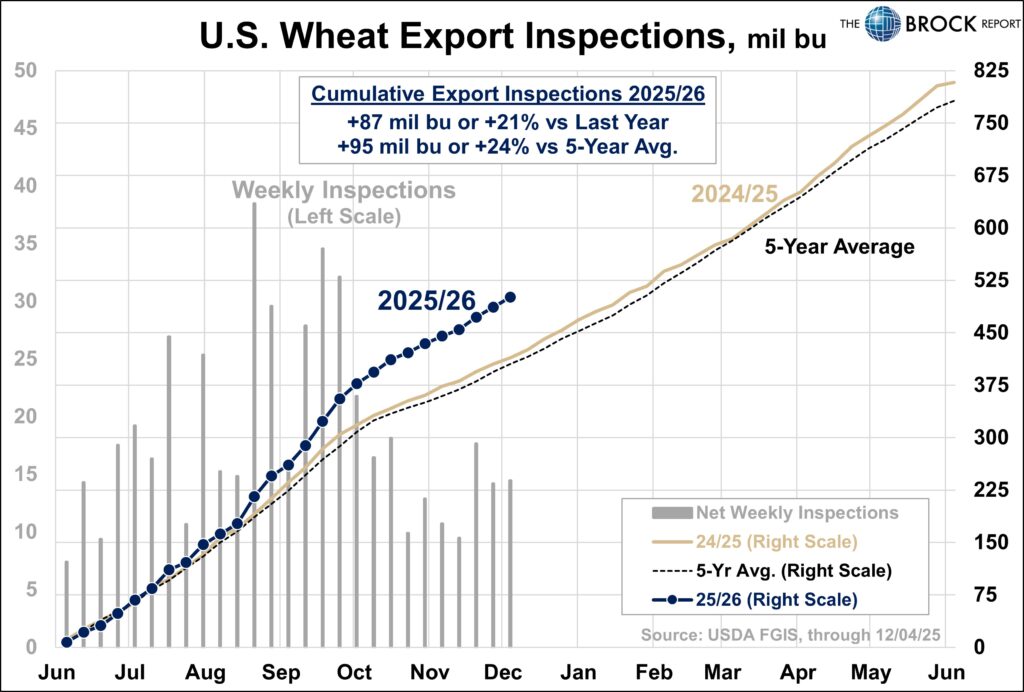

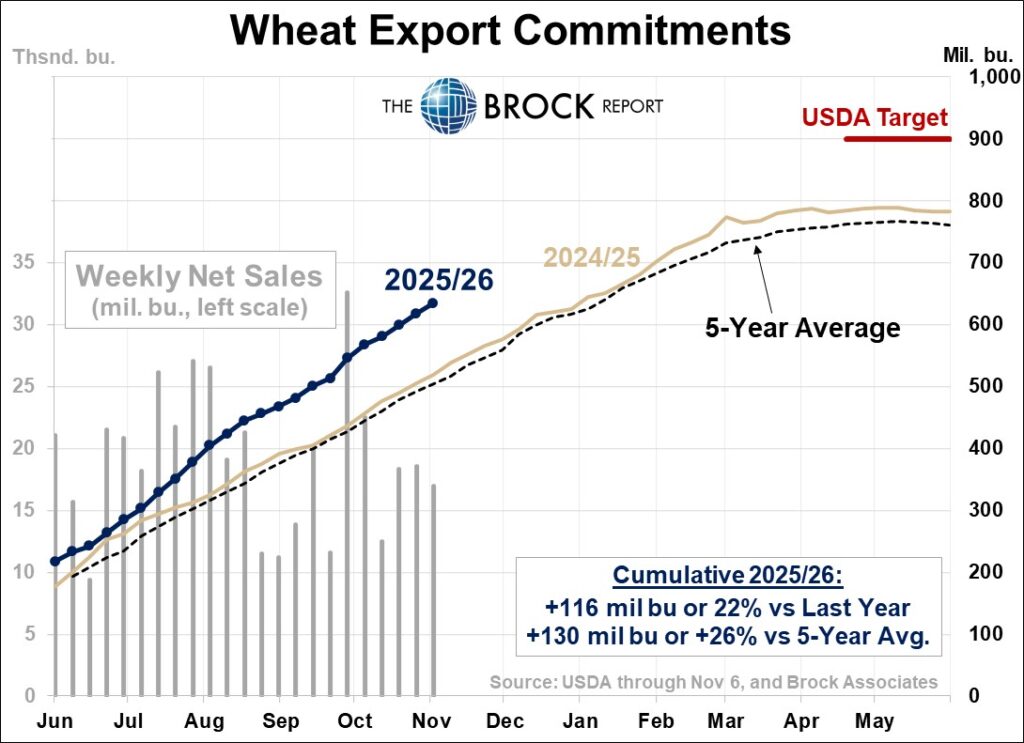

USDA this morning reported net U.S. wheat export inspections for the week ended Dec. 4 at 14.5 million bushels, up from 14.2 million a week earlier and 9.1 million a year earlier and at the high end of trade expectations that ranged from 7.5-14.5 million bushels. U.S. wheat export inspections for the marketing year to date totaled 501 million bushels, up 20.9% from a year earlier.

Delayed weekly export sales data for the week ended Nov. 6 released by USDA earlier this morning showed wheat export sales for that week totaled 17.0 million bushels, down slightly from 19.0 million a week earlier. Wheat export sales for the marketing year to date thru Nov. 6 totaled 634.4 million bushels up 22.4% vs. a year earlier.

Moscow-based analysts expect Russia’s December wheat exports to be larger than in 2024. SovEcon estimates December exports will hit 3.9 MMT, up from 3.4 MMT in December 2024, but down from 4.8 MMT in November. IKAR forecasts December exports at 4.5 MMT. Railway operator Rusagrotrans estimated December wheat exports at 4.3 MMT, based on information about ship arrivals.

Looking to tomorrow’s USDA report, analysts on average see the domestic carryout being cut to 890 million, from 901 million last month. Estimates range from 846 million to 901 million in a Reuters poll. Our own estimate for that survey was 901 million. The world carryout is on average expected to rise slightly to 272.78 MMT, from 271.43 MMT last month.

COTTON AND RICE COMMENTS

NO NEW RECOMMENDATIONS

Cotton futures could not hold on to early strength and settled lower for the sixth straight session on pressure from outside markets and technical selling. December closed down 25 points to 61.88. March closed down 25 points to 63.68, after trading a range of 63.67 to 64.53. May cotton settled down 24 points to 64.76. A drop in crude oil today as well as the stock market set a negative tone for cotton.

Technically, not only is it the sixth straight session lower, it is the third straight day the market settled near session lows, and futures made a new two-week low. March cotton also posted a bearish outside day down. At this point the question is whether the market will take out the contract low of 63.11 in the March, set last month. The answer could depend on what USDA says in its Supply and Demand report tomorrow.

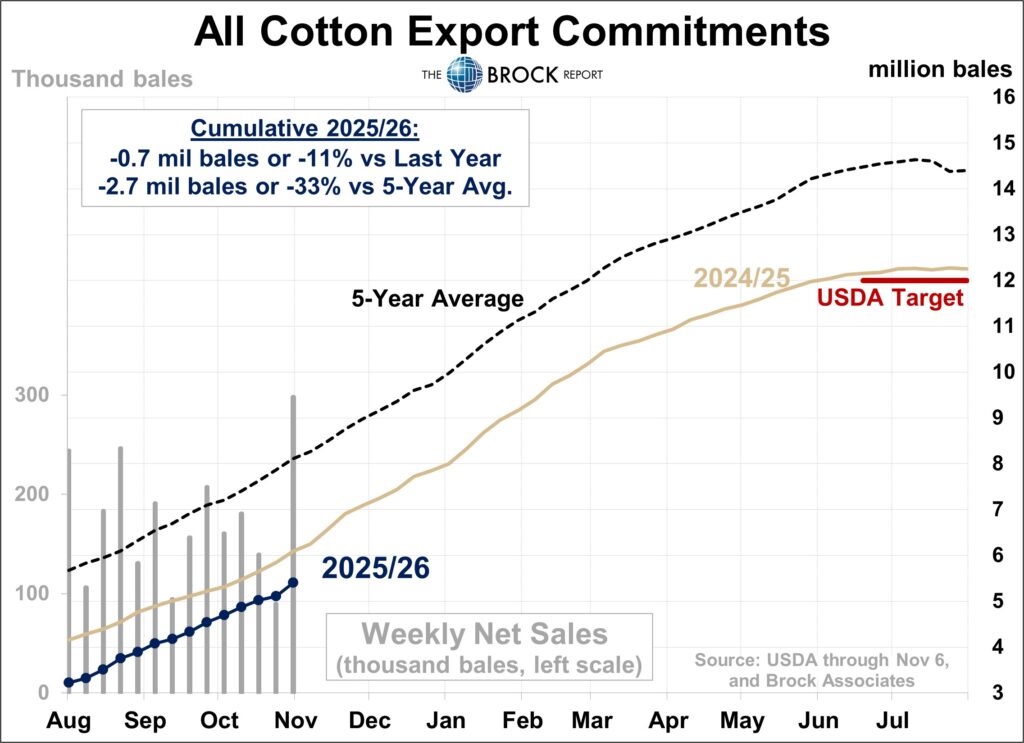

Export sales for the week ended Nov. 6 were a bright spot. USDA reported net sales of 292,100 bales for 2025-26. Vietnam was the top buyer, taking almost 200,000. New crop net sales of 96,800 bales were also solid, but virtually all of that was to one buyer, Mexico. China remains a non-factor.

Rice futures settled higher amid short-covering and bottom-picking. January rice was up 16 cents to $10.14 1/2, after trading a range of $9.98 ½ to $10.21. The contract low, set last week, is at $9.83. March rice settled up 17 cents to $10.46.

Abundant world supplies and soft demand hang over the market. At President Trump’s announcement of a $12 billion aid package today, a rice miller in Louisiana told Trump that while a new deal with Japan has given a big boost to California rice producers, southern producers continue to be harmed by “dumping” of rice in the U.S. by Asian countries including Thailand and India. While we would not expect this to result in any action, Trump did take note of the concerns, so it’s possible we get a Trump pronouncement on rice tariffs at some point.

LIVESTOCK COMMENTS

NO NEW RECOMMENDATIONS

Lean hog futures posted further gains ranging from 12 to 65 cents with nearby Dec. strongest. Most-active Feb. futures gained 13 cents to $82.40, while June futures rose 48 cents to $99.13 on support from technically-driven buying/short covering and stable cash prices.

This was a very quiet day in the hog futures market, with most-active Feb. and April consolidating inside of their Friday ranges, but finishing near their session highs. However, the more deferred contracts all pushed to new highs for the current rally. Feb. lean hog futures still need to finish above their November high of $83.60 to confirm a major price low. June hogs, however, have already moved to their highest level since Oct. 28 and the next significant resistance on the June chart is near $101.50.

Weaker cash fundamentals may weigh on lean hog futures on Tuesday morning. The composite pork cutout value wound up 88 cents lower at $95.51. The national avg. negotiated cash carcass price was $1.49 lower at midafternoon at $70.04. Today’s estimated slaughter topped expectations at 494,000 head, up 12,000 from last week and up 8,000 from last year.

Live cattle futures finished anywhere from $1.23 lower to 18 cents higher under apparent pressure from speculative profit taking in the wake last week’s gains amid uncertainty about cash price direction. Feb. live cattle fell 48 cents to $226.68, while April cattle fell $98 cents to $226.70. Feeder cattle futures $2.53 to $3.40 lower under pressure from profit taking, with Jan. futures falling $3.40 to $335.65 and Mar. falling $2.88 to $330.43.

Most-active Feb. live cattle futures reached an 18-session high this morning, but faded to finish below midrange for the day. Feb live cattle now have nearby chart resistance at $228.03-$228.18, with nearby support at $225.70. Further resistance is at $231.38. April live cattle have chart resistance at $227.75 and $230.45, with nearby support at $225.40 and $224.93. Jan. feeder cattle futures traded failed below their Friday high and posted their lowest close in 3 sessions. Jan. feeders have nearby resistance at $339.13-$340.08, with nearby chart support at $333.38.

Plains direct cash markets stayed quiet today as is normal for a Monday. No packer bids or feedlot asking prices have been established. We would expect steady to higher trade this week due to winter weather and tightening market-ready cattle supplies. Southern Plains feedlots may ask $228 or more for live cattle up from last week’s mostly $225-$226 trade. USDA reports last week’s Kansas negotiated cash trade totaled 3,144 head, at $215-$226, mostly $225-$226. Nebraska weekly negotiated trade totaled 23,264 head at $220-$225 on a live basis and $340-$345 on a dressed carcass basis. Both live and dressed prices were up $10-$15 vs. a week earlier.

Beef cutout values ranged from 30 cents lower to $1.21 higher, with the choice cutout at $360.90.

BROCK MARKET POSITIONS

CORN: Cash-only Marketers: 2024 CROP:100% sold on hedge-to-arrive contracts and regular forward contracts (7-19-23, 8-15-23, 1-2-24, 5-8-24, 5-15-24, 5-16-24, 5-30-24, 11-12-24, 12-12-24, 2-5-25, 2-21-25, 6-5-25, 6-20-25).

2025 CROP: 35% sold on hedge-to-arrive contracts (2-5-25, 2-24-25, 6-9-25, 7-9-25).

Hedgers: 2024 CROP: 100% sold on hedge-to-arrive and regular forward contracts (7-19-23, 8-15-23, 5-8-24, 5-16-24, 11-12-24, 12-12-24, 2-5-25, 2-21-25, 4-15-2025, 6-5-25, 6-20-25).

2025 CROP: 30% sold on hedge-to-arrive contracts and regular forward contracts (2-5-25, 2-24-25, 6-9-25, 7-9-25); aside futures; short July 2026 $5.40 call options against 10% (6-6-25).

SOYBEANS: Cash-only marketers: 2024 CROP: 100% sold (7-19-23, 8-22-23, 11-16-23, 5-16-24, 10-8-24, 12-18-24, 2-5-25, 2-12-25, 2-26-25, 6-2-25, 6-23-25).

2025 CROP: 50% sold on hedge-to-arrive contracts or regular forward contracts (2-12-25, 6-23-25, 7-9-25, 9-2-25, 11-4-25, 12-1-25).

Hedgers: 2024 CROP: 100% cash sold (7-19-23, 8-22-23, 11-16-23, 5-9-24, 12-18-24, 2-5-25, 2-26-25, 4-15-25, 4-29-25, 6-2-25, 6-23-25).

2025 CROP: 50% sold on hedge-to-arrive contracts or regular forward contracts (2-12-25, 6-23-25, 7-9-25, 9-2-2025, 11-4-25, 12-1-25); short Jan. 2026 soybean futures against 10% (12-1-25).

SRW WHEAT: Cash-only Marketers: 2025 CROP: 80% sold on hedge-to-arrive and regular forward contracts (5-30-24, 6-4-24, 10-15-24, 2-24-25, 6-9-25, 6-10-25, 6-24-25, 11-6-25), aside futures. 2026 CROP: No sales advised.

Hedgers: 2025 CROP: 70% sold on hedge-to-arrive and regular forward contracts (5-30-24, 10-15-24, 2-24-25, 6-9-25, 6-10-25, 6-24-25, 11-6-25);. 2026 CROP: No sales advised.

HRW WHEAT: Cash-only Marketers: 2025 CROP: 80% sold on hedge-to-arrive and regular forward contracts (5-30-24, 6-4-24, 10-15-24, 2-24-25, 6-9-25, 6-10-25, 6-24-25, 11-6-25).

Hedgers: 2025 CROP: 70% sold on hedge-to-arrive and regular forward contracts (5-30-24, 10-15-24, 2-24-25, 6-9-25, 6-10-25, 6-24-25, 11-6-25); aside futures. 2026 CROP: No sales advised.

LEAN HOGS: Aside futures.

LIVE CATTLE: Aside futures and options.

FEEDER CATTLE: Feeder sellers are aside futures and options. Feeder buyers remain aside futures.

MILK: No forward cash sales advised; aside futures.

FEED BUYERS: CORN: 100% of 4th qtr. needs bought in the cash market (5-6-25, 9-17-25). SOYMEAL: 100% of 4th qtr. needs bought in the cash market (7-3-25, 9-17-25)

COTTON: Cash-only Marketers: 2024 CROP: 100% sold (2-12-24, 2-27-24, 4-3-24, 6-27-24, 6-28-24, 3-13-25, 3-18-2025, 4-28-25, 6-24-25, 7-16-25). 2025 CROP: 10% sold in the cash market (9-17-25).

Hedgers: 2024 CROP: 100% cash sold (2-12-24, 2-27-24, 4-3-24, 6-27-24, 3-13-25, 3-18-25, 4-28-25, 6-24-25, -16-25), aside futures: 2025 CROP: 10% sold in the cash market (9-17-25. Aside futures.

RICE: 2024 CROP: 100% sold (5-3-24, 5-8-24, 5-28-24, 5-29-24, 7-15-2024, 7-30-24, 9-24-24, 2-21-25. 4-29-25, 7-18-25). 2025 CROP: 10% forward contracted (6-9-25).