GRAIN COMMENTS

CASH COTTON REMINDER: Hedgers and cash-only marketers should lower the previous limit sell order to 66.00. Our earlier recommendation advised selling 10% of 2025 production in the cash market using a good-until-canceled limit order at 66.50 cents on March 2026 cotton futures. This order continues to be good-until-canceled.

Grain and oilseed futures are mixed at mid-session: Soybeans are up 10 to 12 points, boosted by a series of positive demand announcements this morning on exports, biofuels and the NOPA crush. It is being led by soybean oil, which has surged by more than 175 points. Corn and wheat however are both down slightly and at the day’s lows as of 11 a.m. CT. Cotton is also slightly lower. Rice is flat.

In outside markets, crude oil remains in retreat, down nearly $3 as worries fade about an imminent U.S. attack on Iran. Stocks are higher, with the Dow up 400 points, and the dollar index is up 0.2%. Gold is down $25.

The EPA plans to finalize 2026 biofuel blending quotas by early March, while dropping a plan to penalize imports of renewable fuels and feedstocks, Reuters reported this morning. The would represent a partial compromise between oil and ag groups, preserving increased blending targets announced last year while abandoning the plan to disincentivize imports of used cooking oil, which refiners had opposed. EPA in June had proposed total biofuels blending volumes of 24.02 billion gallons in 2026 and 24.46 billion in 2027, up from 22.33 billion in 2025. The total included a target of 5.61 billion for biobased diesel, but EPA is not considering a range of 5.2 to 5.6 billion gallons for 2026. Soybean futures and soyoil surged this morning on the news, a reaction we find somewhat confusing given that the adjustments reported today are not bullish versus what was proposed last summer. But Reuters noted today that it had previously reported that EPA was considering delaying its entire proposal by a year, so from that standpoint today’s report could be a relief to the biofuels industry.

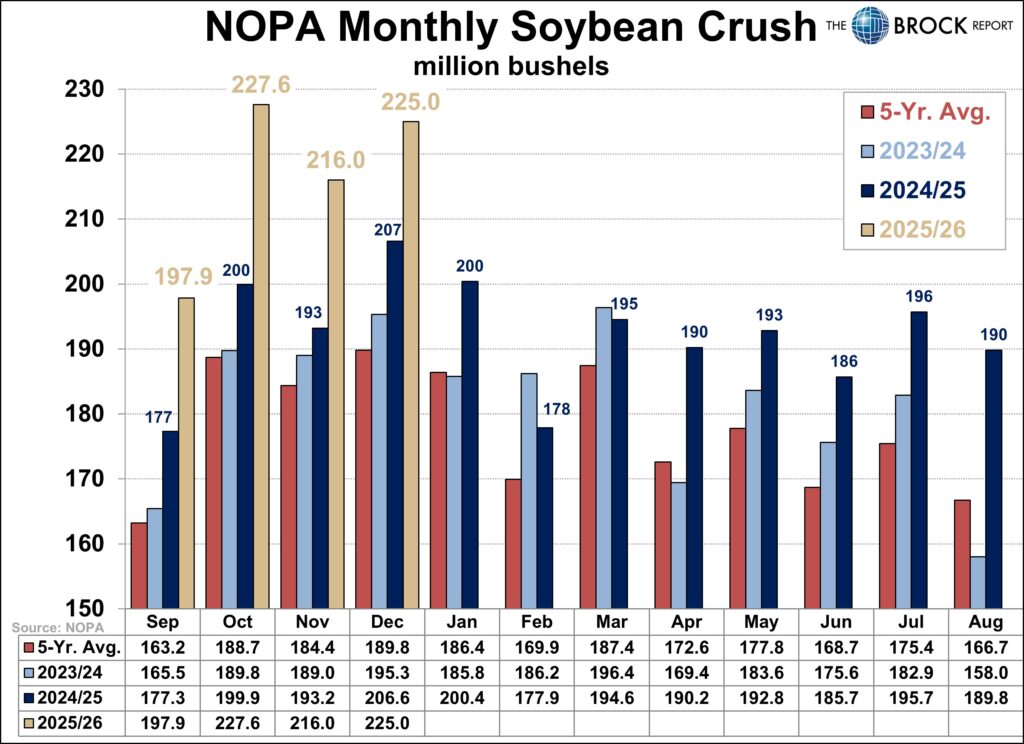

The NOPA crush report just out shows the December crush at 224.991 million bushels, up 4.1% from a month earlier, 8.9% from a year ago, and above the average Reuters survey estimate of 224.809 million. It is the second largest monthly crush on record. Soybean oil stocks of 1.642 billion pounds were up 8.5% from November and 32.8% from a year ago, but below the average survey estimate of 1.686 billion pounds.

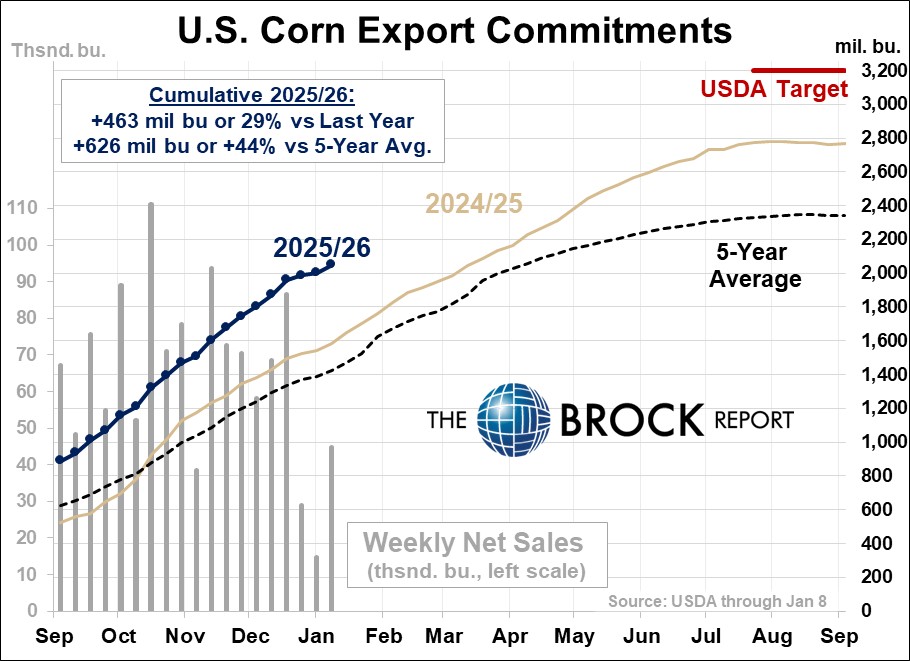

As noted this morning the export news for corn and soybeans this morning, and all week, was positive for prices. For corn, weekly export sales came in at a net 1.140 MMT, up sharply from last week, but still down 10% from the four-week average. Trade guesses had ranged from 600,000 to 1.4 MMT. Meanwhile, USDA reported two sizable flash sales: 500,302 metric tons to unknown destinations, and 260,000 metric tons to Japan.

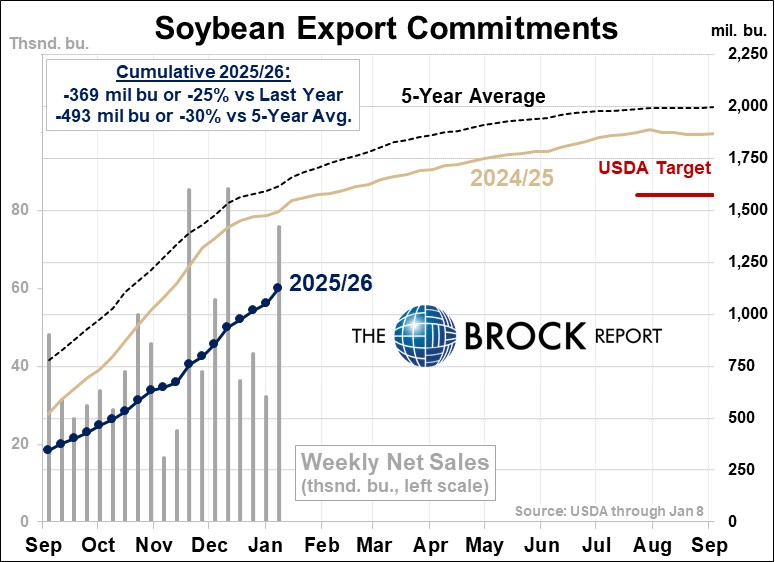

For soybeans, weekly net export sales were strong at 2.062 MMT, topping trade guesses that ranged from 800,000 to 1.8 MMT, and up 54% from the four-week average. China accounted for 1.2 MMT of the total. USDA also reported three flash export sales for soybeans: 435,000 metric tons of soybeans “received during the reporting period” to unknown destinations; another sale of 110,000 metric tons to unknown; and 204,000 metric tons to China.

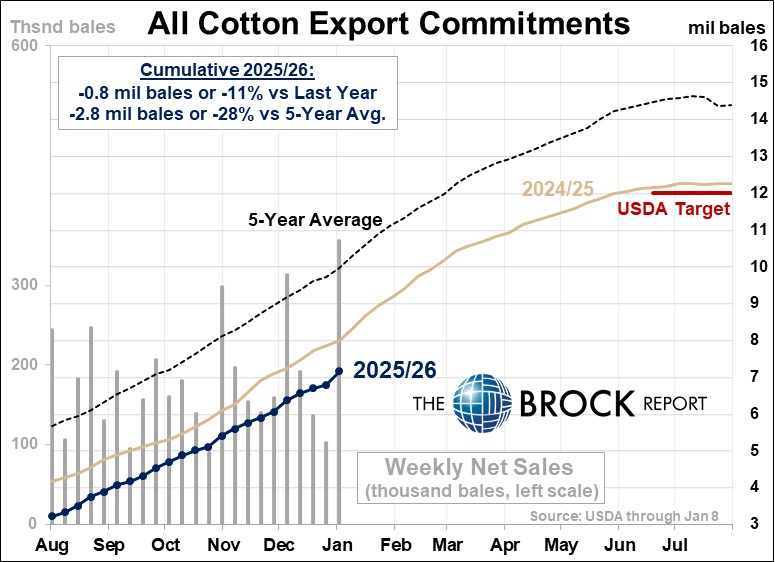

Cotton weekly export sales were also bullish this morning. USDA reported net sales of 339,700 bales, a marketing year high and up 89% from the four-week average. Vietnam remains the top buyer, but China, which has been consistently buying modest totals of about 10,000 bales recently, upped that total to 57,200 bales in this morning’s report. Weekly cotton shipments meanwhile came in at 156,100 bales, up 8% from the four-week average.

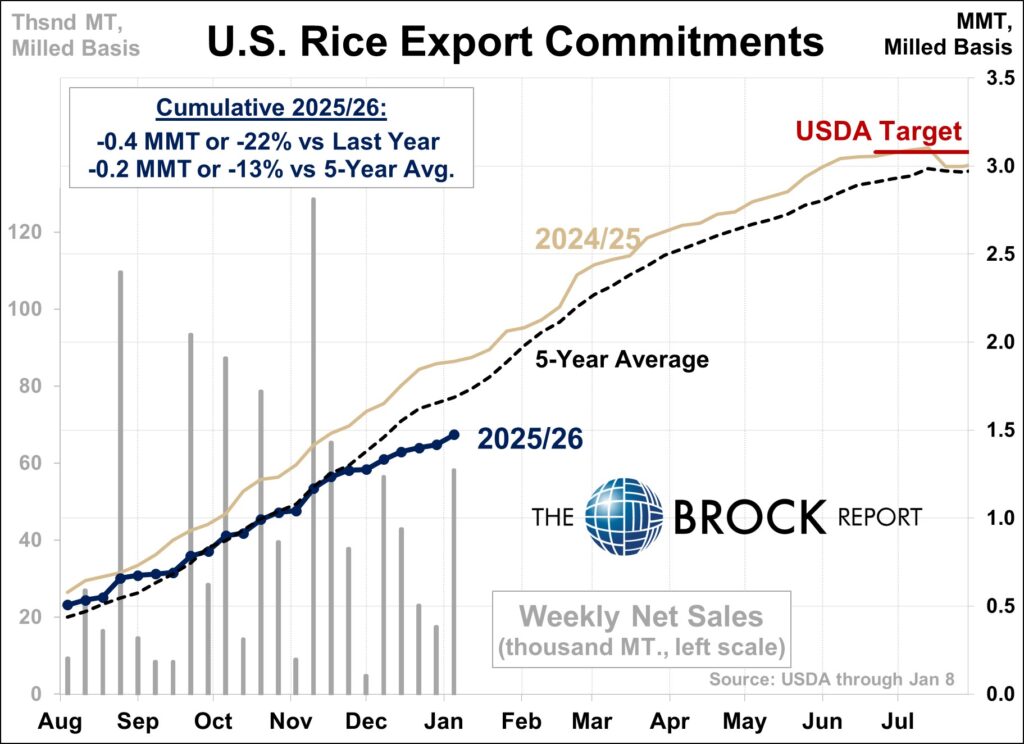

USDA reported rice net export sales of 58,100 metric tons, up 66% from the four-week average. Of that total, 40,400 metric tons was long-grain, to Mexico and unknown destinations. Weekly rice export shipments of 40,500 metric tons were up 13% from the four-week average.

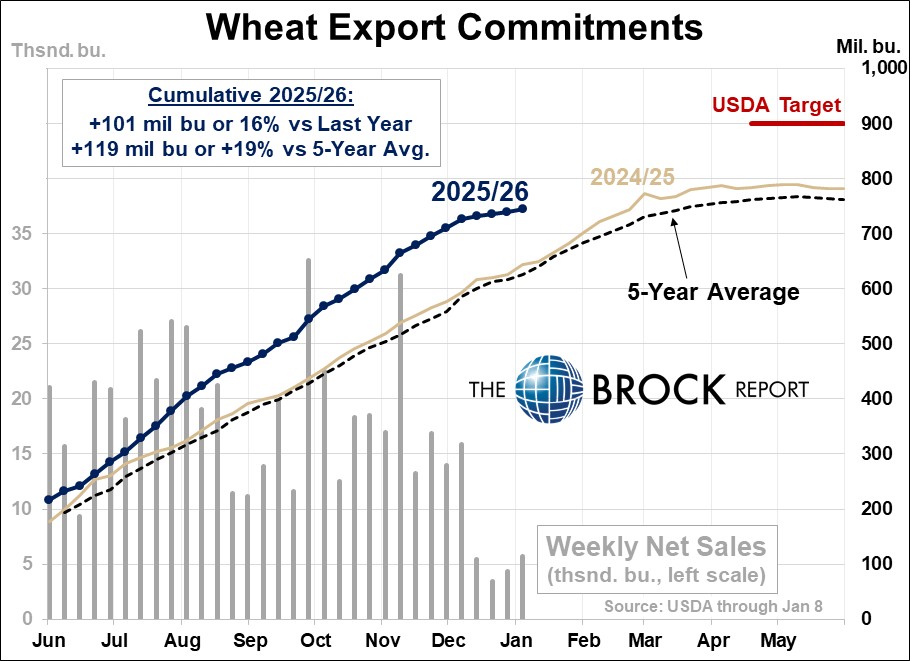

Wheat futures have shown limited movement since reopening this morning with large supplies and stiff export market competition keeping pressure on prices. Prices have traded in narrow ranges of just 6 1/4 cents since reopening on Wednesday evening.

Another low weekly U.S. export sales total provided evidence of stiff export market competition. Net wheat export sales for the week ended Jan. 8 came in at just 5.7 mil. bu., up just slightly from the previous week’s sales of 4.1 mil. bu. and trade expectations that ranged from 3.5-14.5 mil. bushels.

U.S. wheat export sales for the marketing year to date thru Jan. 8 were still 15.6% above a year earlier. However, sales for 2025-26 delivery over the past 4 weeks total just 19 mil. bu., down sharply from 62.4 mil. bu. for the same 4 weeks a year ago. USDA reported sales have now fallen below the seasonal pace needed to reach USDA’s current 2025-26 export forecast of 900 mil. bu., although export shipments remain ahead of pace to reach that target.

LIVESTOCK COMMENTS

ADVICE REMINDER: HOG HEDGERS were earlier advised to:

- Buy April 2026 Lean Hog futures at the market on 25% of 1st qtr. marketings to exit the current short position.

- Buy June 2026 Lean Hog futures at 105.500 stop-close-only on 25% of 2nd qtr. marketings to exit the current short position.

Livestock futures are higher across the board at 11:25 a.m. CT, with lean hog futures ranging from 45 cents to $2.13 higher, while live cattle futures are 58 cents to $1.30 higher and feeder cattle futures are $2.15 to $3.23 higher. Front-end lean hog futures are strongest on further support from indications of strong demand and technically-driven buying. Live cattle futures have recovered on support from a continued strong cash market tone amid reduced offerings. Feeder cattle futures also continue to find support from strong cash markets and technical strength.

Nearby Feb. lean hog futures have broken out to a 3-month-plus high of $87.48, while April futures have charted a new contract high of $94.75 and June futures have charted a new high of $106.55. Given this strength, we see no reason to be short April futures at this time and we want to exit our June futures hedge as well if the market finishes strongly today. We will maintain our hedges in Aug. futures on 25% of 3rd and 4th qtr. marketings for now, but will likely be quick to exit these positions if the market continues to show strength. Hedgers should stay alert for possible fresh advice on Friday.

The composite pork cutout value was $1.96 higher at midmorning at $93.25. USDA again did not report midmorning negotiated cash carcass values due to packer confidentiality reasons. The weighted avg. price of hogs sold under swine/pork market formula agreements at midmorning was $80.37, up 11 cents vs. Wednesday morning. The lagging CME cash lean hog index is 11 cents lower at $80.39, and is expected to fall another 11 cents on Thursday. Today’s hog slaughter is expected to run 493,000 head, up 8,000 from last week, and 9,000 vs. last year. The avg. pork packer operating margin is estimated by HedgersEdge at $15.45 per head, down from $16.90 on Wednesday.

Feb. live cattle futures have traded a relatively narrow range of $1.25 inside of their Wednesday trading range and now have nearby chart resistance at $236.20 and $237.55, with nearby support at $234.63-$234.95. April live cattle are also trading an inside day, with nearby chart resistance at $238.55 and $239.05 and nearby support at $236.75-$237.23. As we thought, Wednesday’s weakness in feeder cattle futures appears to have been just a bull-market correction. Most-active Mar. feeder cattle futures have charted a new 12-week high of $363.38 and are sitting just below that level after establishing nearby chart support at $359.33.

There is still nothing going on in Plains direct cash cattle markets this morning with neither packer bids nor feedlot asking prices established. We would expect packer enquiries to pick up later today, but right now it is looking like significant trade may be delayed until Friday. Steady to higher trade is still favored. Beef cutout values were $1.91 to $2.28 higher at midmorning, with the choice cutout value at $360.44. The avg. beef packer operating margin is estimated by HedgersEdge at minus $198.75 per head up from minus $202.75 on Wednesday.

BROCK MARKET POSITIONS

CORN: Cash-only Marketers: 2024 CROP:100% sold on hedge-to-arrive contracts and regular forward contracts (7-19-23, 8-15-23, 1-2-24, 5-8-24, 5-15-24, 5-16-24, 5-30-24, 11-12-24, 12-12-24, 2-5-25, 2-21-25, 6-5-25, 6-20-25).

2025 CROP: 40% sold on hedge-to-arrive contracts (2-5-25, 2-24-25, 6-9-25, 7-9-25, 1-9-26).

Hedgers: 2024 CROP: 100% sold on hedge-to-arrive and regular forward contracts (7-19-23, 8-15-23, 5-8-24, 5-16-24, 11-12-24, 12-12-24, 2-5-25, 2-21-25, 4-15-2025, 6-5-25, 6-20-25).

2025 CROP: 40% sold on hedge-to-arrive contracts and regular forward contracts (2-5-25, 2-24-25, 6-9-25, 7-9-25, 1-9-26); aside futures; short July 2026 $5.40 call options against 10% (6-6-25).

SOYBEANS: Cash-only marketers: 2024 CROP: 100% sold (7-19-23, 8-22-23, 11-16-23, 5-16-24, 10-8-24, 12-18-24, 2-5-25, 2-12-25, 2-26-25, 6-2-25, 6-23-25).

2025 CROP: 50% sold on hedge-to-arrive contracts or regular forward contracts (2-12-25, 6-23-25, 7-9-25, 9-2-25, 11-4-25, 12-1-25).

Hedgers: 2024 CROP: 100% cash sold (7-19-23, 8-22-23, 11-16-23, 5-9-24, 12-18-24, 2-5-25, 2-26-25, 4-15-25, 4-29-25, 6-2-25, 6-23-25).

2025 CROP: 50% sold on hedge-to-arrive contracts or regular forward contracts (2-12-25, 6-23-25, 7-9-25, 9-2-2025, 11-4-25, 12-1-25), aside futures, long $10.50 February put options on Mar. 2026 futures against 20% (1-9-26).

SRW WHEAT: Cash-only Marketers: 2025 CROP: 80% sold on hedge-to-arrive and regular forward contracts (5-30-24, 6-4-24, 10-15-24, 2-24-25, 6-9-25, 6-10-25, 6-24-25, 11-6-25), aside futures. 2026 CROP: No sales advised.

Hedgers: 2025 CROP: 70% sold on hedge-to-arrive and regular forward contracts (5-30-24, 10-15-24, 2-24-25, 6-9-25, 6-10-25, 6-24-25, 11-6-25);. 2026 CROP: No sales advised.

HRW WHEAT: Cash-only Marketers: 2025 CROP: 80% sold on hedge-to-arrive and regular forward contracts (5-30-24, 6-4-24, 10-15-24, 2-24-25, 6-9-25, 6-10-25, 6-24-25, 11-6-25).

Hedgers: 2025 CROP: 70% sold on hedge-to-arrive and regular forward contracts (5-30-24, 10-15-24, 2-24-25, 6-9-25, 6-10-25, 6-24-25, 11-6-25); aside futures. 2026 CROP: No sales advised.

LEAN HOGS: Short April 2026 lean hog futures against 25% of 1st qtr. marketings (1-12-26), June 2026 lean hog futures against 25% of 2nd qtr. marketings (1-12-26) and Aug. 2026 lean hog futures against 25% of 3rd and 4th qtr. marketings (1-12-26). Long January $81 put options on Feb. 2026 lean hog futures (12-17-25), short $108 call options against June 2026 lean hog futures (1-2-26). Aside futures.

LIVE CATTLE: Aside futures and options.

FEEDER CATTLE: Feeder sellers are aside futures. Feeder buyers remain aside futures.

MILK: No forward cash sales advised; aside futures.

FEED BUYERS: CORN: No forward cash purchases advised. SOYMEAL: 100% of 1st qtr. needs bought in the cash market; 50% of 2nd qtr. needs bought in the cash market (1-7-26).

COTTON: Cash-only Marketers: 2024 CROP: 100% sold (2-12-24, 2-27-24, 4-3-24, 6-27-24, 6-28-24, 3-13-25, 3-18-2025, 4-28-25, 6-24-25, 7-16-25). 2025 CROP: 10% sold in the cash market (9-17-25).

Hedgers: 2024 CROP: 100% cash sold (2-12-24, 2-27-24, 4-3-24, 6-27-24, 3-13-25, 3-18-25, 4-28-25, 6-24-25, -16-25), aside futures: 2025 CROP: 10% sold in the cash market (9-17-25). Aside futures.

RICE: 2024 CROP: 100% sold (5-3-24, 5-8-24, 5-28-24, 5-29-24, 7-15-2024, 7-30-24, 9-24-24, 2-21-25. 4-29-25, 7-18-25). 2025 CROP: 10% forward contracted (6-9-25).