Wheat futures have surged this week as concerns about poor U.S. winter wheat conditions have risen amid continued drought conditions in key HRW wheat growing areas. The market may be getting ahead of itself, as it is still too early in the spring growing season to count on a significant crop disaster — only 11% of the U.S. winter wheat crop was headed as of April 12. We know wheat has significant recuperative abilities — that’s why they say: “Wheat is a weed.” And a fast-developing El Nino weather phenomenon could bring needed rains to dry areas later this spring. However, at this point, odds are high we will not see another above-trend winter wheat yield as we did both 2024 and 2025.

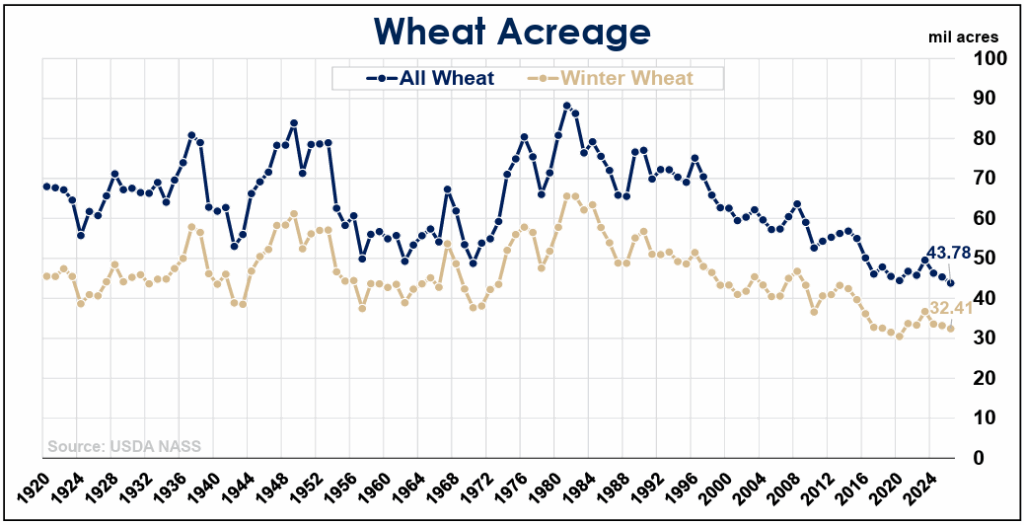

There is more concern about U.S. wheat yields this year, with U.S. all-wheat seedings forecast to be the lowest since 1919 at 43.78 million acres, down about 2.5 million from two years ago. HRW wheat seedings are estimated to be down 743,000 acres from last year. “Other” spring wheat planting intentions, mostly hard red spring wheat, are down 575,000 acres or 6% versus last year and 1.26 million acres from 2024, although the price rally since late February and surging fertilizer prices may have attracted some additional acres from corn.

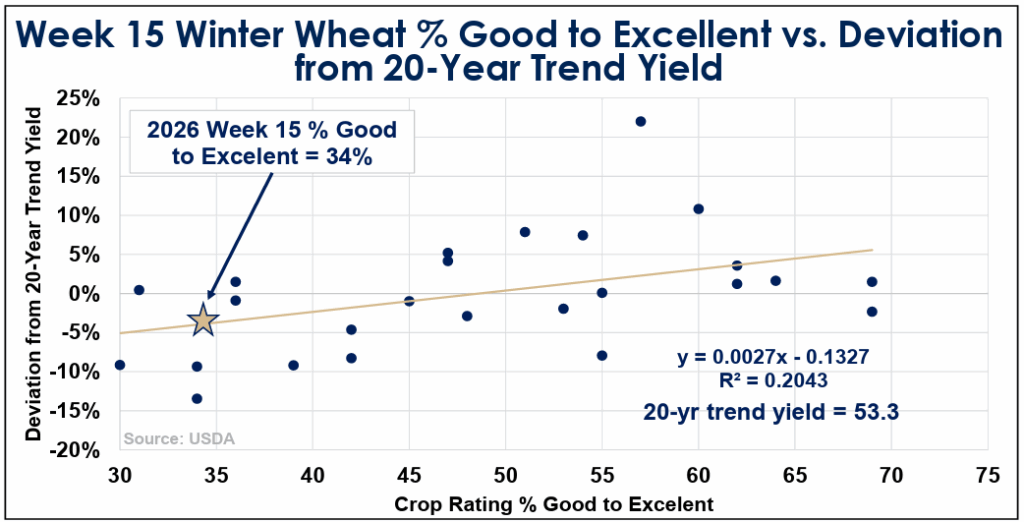

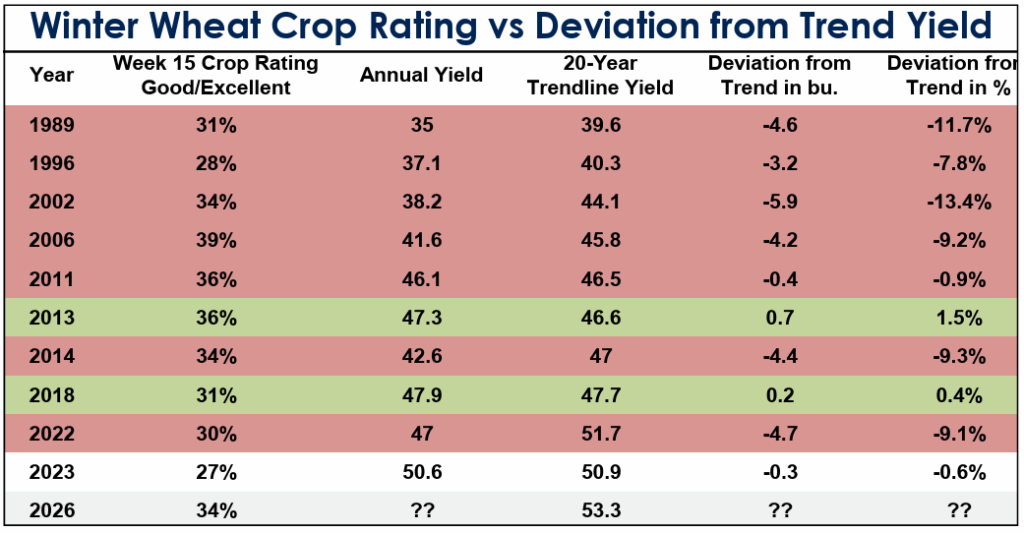

The April 12 U.S. winter wheat crop rating of 34% good/excellent represented the sixth lowest rating for week 15 of the year in USDA data going back to 1986. Condition ratings at this time of the year do not correlate closely with final yields. However, as we can see in the table below, in 10 previous years when the crop was rated below 40% good/excellent as of week 15, the U.S. winter wheat yield wound up below the 20-year trendline eight times and was substantially below trend in six of those years. In both 2013 and 2018, the crop recovered and the average yield wound up slightly above trend. The 40% good/excellent level is an arbitrary cut-off point, but a logical one. The worst-case scenario, if conditions stay poor, would seem to be a winter wheat yield 7.8% to 13.4% below the 20-year trend, which this year would be 46.2 to 49.1 bushels, while the best-case scenario would be a yield of 53.0 to 54.1 bushels. A worst-case outcome could mean higher prices, while a best-case outcome would likely mean prices significantly below current levels.

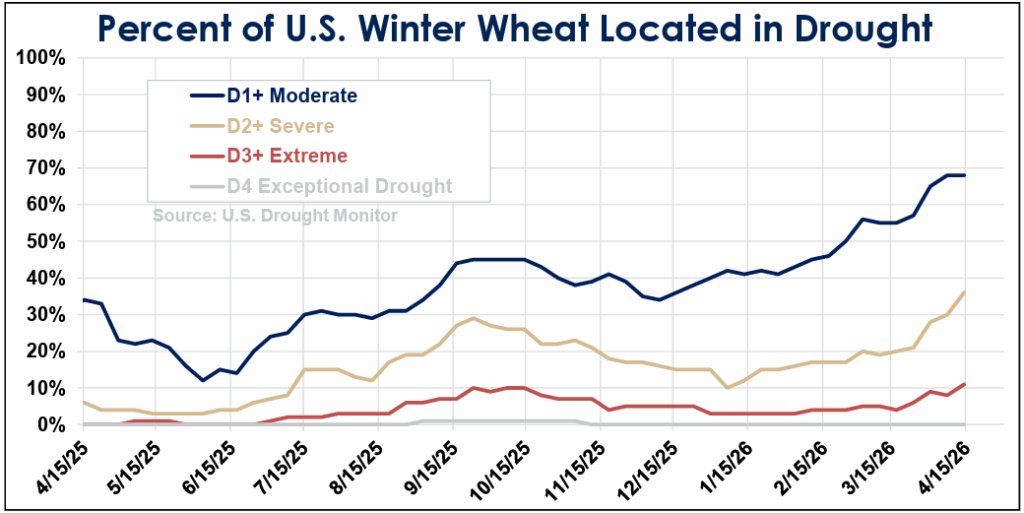

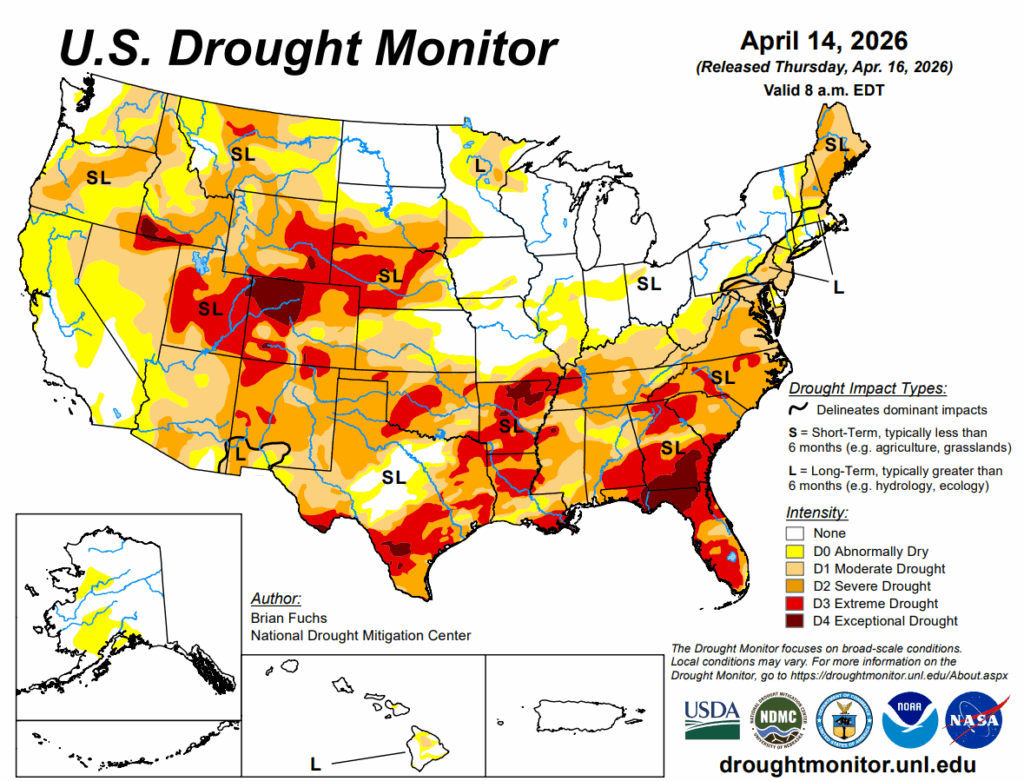

Continued dry weather would also likely boost acreage abandonment. The portion of U.S. winter wheat area under moderate or more intense drought has surged to 68% as of April 14 from 42% at the start of 2026, and just 34% a year ago. This included 100% of Colorado wheat area, 94% of Nebraska area, 90% of Montana area, 83% of Texas area and 68% of Kansas area. Drought is also a problem in northwest white wheat states, while most major SRW wheat states are in good shape moisture-wise.