GRAIN COMMENTS

CORN RECOMMENDATION: Replace the existing March 2027 Corn good-til-cancelled buy stop at 464.00 with a new buy stop at 461.00 good-til-cancelled to exit the remaining 15% hedge.

Grain and oilseed futures are mostly lower at mid-day: Soybeans are down 2 to 4 cents, and wheat is down 8 to 10. Cotton is down slightly, and corn is up 1 to 2 cents. Traders are eying the Midwest weather outlook, which includes a lot of heat and little rain over the next 10 days, while getting ready for Tuesday’s USDA acreage and grain stocks reports.

In outside markets, major U.S. stock indexes are up slightly. The University of Michigan’s monthly consumer sentiment survey showed a notable improvement from last month’s recent recent low, as a softening of gas prices eases pain at the pump. Crude oil is down another $2.50 this morning. The dollar index is down 0.15%.

Starting this weekend and through at least next week, temperatures will rise into the 90s in much of the Midwest, and rainfall after this weekend looks to be limited. The west-central and northwest Corn Belt look to be the biggest concern, as much of that region is already too dry. Areas of concern include western Iowa, eastern South Dakota, Nebraska and parts of Minnesota, World Weather Inc. says. Some storms are possible in this region on Saturday, but after that heat and dryness could persist for 10 days.

Elsewhere, the heat could still do more good than harm given the generally favorable soil moisture situation in place and the need for more growing degree days. As of Tuesday most of the Midwest region was drought-free in the weekly Drought Monitor. It showed 35.6% of the region as abnormally dry and 13.3% in moderate drought, with much of that area is Kentucky and far southern Illinois.

Corn conditions in France are deteriorating amid a historic heatwave. The crop was 76% good/excellent as of Sunday, down eight points from the prior week. And further declines are likely with France this week reporting all-time high temperatures.

Wheat futures remain solidly lower at midsession, with pressure on prices coming from renewed weakness in crude oil futures, fading concerns about the heat wave in Europe, prospects for an active weekend of winter wheat harvesting and technically-driven selling/long liquidation. However, after accelerating lower in the first 20 minutes after reopening this morning, futures have gradually worked their way back near midrange for the session.

Most-active September soft red wheat futures earlier traded to an 8-session low of $5.845 but are now near $5.92, with nearby chart resistance at $6.005. September hard red winter wheat futures earlier traded to a 2.5 month low of $6.15, but are now near $6.22, with nearby chart resistance at $6.2975.

Nearby September milling wheat futures on the Euronext Exchange in Paris are about 1.8% lower at a 4-session low as the heat wave across western Europe is due to ease over the weekend. The current temperature in Paris is 96 F., but high temperatures are expected to be near 80 F. next Monday thru Friday.

LIVESTOCK COMMENTS

NO NEW RECOMMENDATIONS

Livestock futures are mixed at 11:50 a.m. CT, with lean hog futures 8 cents to $1.23 higher, while live cattle futures are 40 cents to $1.68 lower and feeder cattle futures are $3.708 to $4.05 lower.

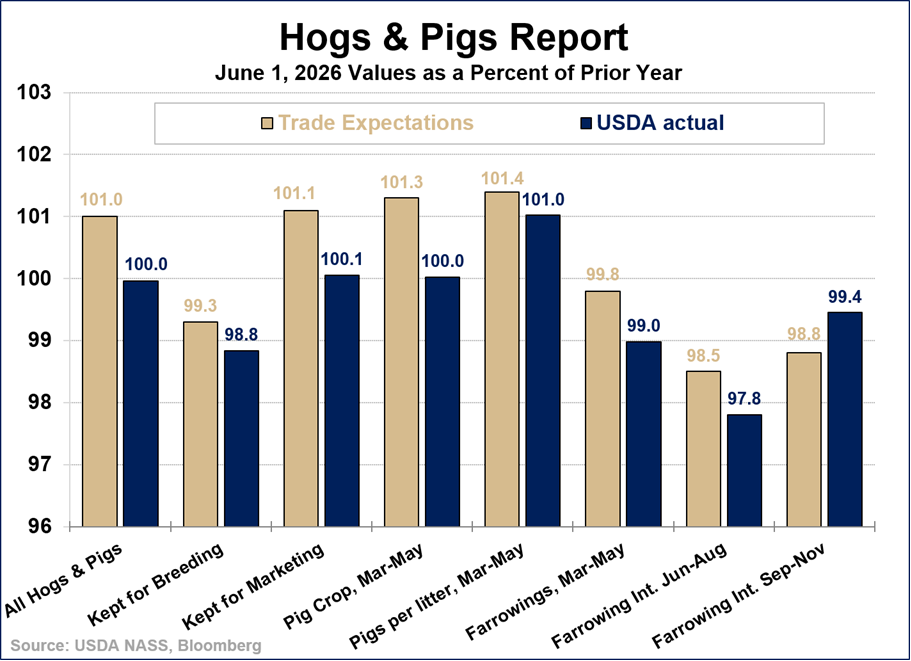

Lean hog futures have been boosted by Thursday afternoon’s Hogs and Pigs report, which pegged U.S. hog supplies virtually unchanged from a year earlier and slightly below trade expectations. Live cattle futures have been pressured by pre-weekend speculative position evening amid a continued lack of trade in Plains direct cash markets. Feeder cattle futures have been pressured by speculative position evening and live cattle market weakness despite Thursday’s $6.03 jump in the CME cash feeder cattle index to a new all-time high.

July and August lean hogs have found limited price support from the USDA report, but October and more deferred contracts are solidly higher. Oct. appears to have confirmed a significant low after gapping higher on this morning’s open and trading to a 13-session high of $82.58, however, the market has backed off near midrange for the day. Nearby support for October is at $81.60-$81.65.

Cash market fundamentals are mixed. The midmorning composite pork cutout value was $2.60 higher at $97.82 but the weighted average price of hogs sold under swine/pork market formula agreements was $89.01, down $1.18 versus Thursday morning. Today’s hog slaughter is expected to run 456,000 head, down 5,000 from a year ago, while the Saturday slaughter is expected to run 55,000 head, steady with last year.

Most-active August live cattle futures have fallen back against nearby chart support at $245.50 after establishing nearby resistance at $247.25. The support is holding so far for a fourth straight session. Downside for August should be limited by the fact it is about $13-$15 discount to last week’s Plains cash trade. August feeder cattle futures have traded as low as $368.50 after establishing nearby resistance at $373.53. Nearby support is at $367.13-$367.50. August feeders are now more than $12 discount to cash.

Plains direct cash cattle markets remain quiet this morning, but packers have posted bids of $255-$256 live and $408 on a dressed carcass basis in Nebraska, with bids at $255 live also reported in Texas and Colorado. Feedlots continue to pass on those bids and are reportedly asking $415 on a dressed basis in Nebraska. Beef cutout values ranged from $2.33 to $4.22 lower at midmorning, with the choice cutout at $392.10, which will put increased pressure on packer margins.

USDA has confirmed another 5 cases of New World Screwworm (NWS) in Texas, all in sheep, bringing the total number of cases to 25, 24 of which have been in Texas.

Click Here to View THE BROCK REPORT Position Monitor

NOTE: Along with the potential for profit, there is always a risk of losing money when trading futures and options contracts.

Copyright 2026 by Richard A. Brock & Associates, Inc.

Any unauthorized redistribution or reproduction of this commentary is strictly forbidden.